This briefing is designed for financial advisers only and should not be distributed to or relied upon by individual investors.

This briefing is designed for financial advisers only and should not be distributed to or relied upon by individual investors.

Aidan Golden

Head of Group Technical Services

Welcome to the Spring 2026 edition of NAVIGATOR.

The pace of change facing advisers continues to accelerate. Client mobility is increasing, private and complex assets are becoming mainstream, and regulatory scrutiny is intensifying. In this environment, planning in silos is no longer fit for purpose.

This edition’s Technical Spotlight focuses on why life insurance sits at the centre of holistic wealth planning. Brendan Harper opens the section by examining why fragmented planning so often breaks down when wealth structures cross borders, and why advisers are increasingly turning to integrated, portable solutions. The country articles and Case Study Insights that follow show how this plays out in practice.

That theme is reinforced in our Country Focus piece by Benjamin Fiorino, which explores the France–Monaco corridor and demonstrates why residency led planning is rarely sufficient on its own. Instead, advisers must reconcile tax, civil law and family dynamics within a coherent structure that continues to work over time.

In Navigator Voices, I speak with Stephen Atkinson, who reflects on how supervisory expectations are evolving as private market assets and more sophisticated strategies move into the mainstream. His message is reinforced by Brendan Harper’s article on why insurer credit ratings matter more than ever for securities backed lending, set against recent correspondence from the Luxembourg financial regulator (CSSF). Together, these developments underline the growing importance of insurer capability in an increasingly scrutinised environment.

Across this edition, one message is clear. Advisers who adopt holistic, well governed structures will be best placed to deliver resilient outcomes, and to identify new planning opportunities for their clients.

As always, our team is here to support you in delivering the best possible outcomes for your clients.

Thank you for reading.

Aidan Golden

Head of Group Technical Services

Aidan Golden

Head of Group Technical Services

Bienvenue dans l’édition Printemps 2026 de NAVIGATOR.

Le rythme des évolutions auxquelles les conseillers sont confrontés continue de s’accélérer. La mobilité des clients augmente, les actifs privés et complexes deviennent une composante courante des portefeuilles, et la pression réglementaire s’intensifie. Dans cet environnement, une planification en silos n’est plus adaptée.

Le Technical Spotlight de cette édition met en lumière pourquoi l’assurance-vie occupe une place centrale dans une approche globale de la planification patrimoniale. Brendan Harper ouvre cette section en analysant pourquoi une planification fragmentée se fragilise souvent lorsque les structures patrimoniales deviennent transfrontalières, et pourquoi les conseillers se tournent de plus en plus vers des solutions intégrées et portables. Les articles pays et les études de cas qui suivent illustrent concrètement cette approche.

Ce thème est également développé dans notre section Country Focus par Benjamin Fiorino, qui examine le corridor France–Monaco et montre pourquoi une planification fondée uniquement sur la résidence est rarement suffisante. Les conseillers doivent au contraire articuler les enjeux fiscaux, juridiques et familiaux au sein d’une structure cohérente, capable de s’inscrire dans la durée.

Dans Navigator Voices, je m’entretiens avec Stephen Atkinson, qui revient sur l’évolution des attentes des autorités de supervision à mesure que les actifs des marchés privés et les stratégies plus sophistiquées s’inscrivent dans la norme. Ce constat est renforcé par l’article de Brendan Harper consacré à l’importance croissante des notations de crédit des assureurs dans le cadre des prêts sur titres, dans le contexte des récents échanges avec le régulateur financier luxembourgeois (CSSF). Ensemble, ces évolutions soulignent l’importance croissante des capacités des assureurs dans un environnement de plus en plus encadré.

À travers cette édition, un message ressort clairement. Les conseillers qui adoptent des structures globales et bien encadrées seront les mieux placés pour obtenir des résultats durables et pour identifier de nouvelles opportunités de planification pour leurs clients.

Comme toujours, nos équipes sont à votre disposition pour vous accompagner dans la mise en œuvre des meilleures solutions pour vos clients.

Merci de votre lecture.

Aidan Golden

Head of Group Technical Services

Brendan Harper

Head of Asia and HNW Technical Services

Recent correspondence from the Luxembourg financial regulator, the Commission de Surveillance du Secteur Financier (CSSF), has brought renewed attention to how banks should treat securities-backed loans secured by life insurance policies for regulatory capital purposes.

In this article, Brendan Harper examines a regulatory clarification that, while technical, has practical implications for banks, advisers and clients, particularly as insurer credit ratings play an increasingly central role in lending decisions.

Simon Martin

Head of UK Technical Services

From May 2026, paid interaction with HMRC will be subject to a new mandatory registration regime for tax advisers.

In this article, Simon Martin, Head of UK Technical Services, outlines who must register, the standards advisers will need to meet and the practical consequences of non-compliance.

Brendan Harper

Head of Asia and HNW Technical Services

Recent correspondence from the Luxembourg financial regulator, the Commission de Surveillance du Secteur Financier (CSSF), has brought renewed attention to how banks should treat securities-backed loans secured by life insurance policies for regulatory capital purposes.

Securities-backed lending continues to play an important role in private banking, allowing clients to raise liquidity while maintaining long-term investment or planning structures. In Luxembourg, this commonly involves a life insurance policy being pledged or assigned to a bank as security for the loan.

Under the EU Capital Requirements Regulation (CRR), banks must calculate a risk-weighted exposure amount (RWA) for such lending. This determines how much regulatory capital a bank must hold and directly influences lending appetite, pricing and overall loan economics.

Recent engagement from the CSSF has focused on how these rules should be applied where life insurance policies are used as collateral.

Although the CSSF correspondence itself has not been made public, its substance has been confirmed to market participants and advisers. The regulator has reminded certain private banks of the correct application of Article 232 CRR where a life insurance policy is pledged as collateral.

The CSSF has challenged practices where banks apply a “look-through” approach to the underlying assets held within a policy when assessing credit risk. Instead, Article 232 requires banks to substitute the credit risk of the borrower with that of the insurance undertaking issuing the policy.

In practical terms, this means the relevant risk is the credit quality of the insurer, rather than its solvency ratio or the composition of the policy’s underlying investment assets.

This reflects a legal and regulatory reality. In an insurer insolvency scenario, banks do not have direct rights over the insurer’s assets. The regulatory focus therefore rests on the insurer’s financial strength and creditworthiness as counterparty.

A key consequence of this approach is the increasing importance of independent insurer credit ratings.

Under the CRR framework:

By contrast, insurers without an independent credit rating may fall into higher risk-weight categories. This can result in higher capital charges and less competitive loan conditions.

From a regulatory perspective, the CSSF’s clarification reinforces that credit ratings are not simply a marketing credential. They are a relevant input into how banks assess, structure and price securities-backed lending.

For advisers working with high-net-worth or internationally mobile clients, this development is a reminder that structuring decisions can have downstream banking consequences.

Where life insurance is intended to support securities-backed lending:

This is not a change in the law, but a clarification of supervisory expectations. Over time, it may encourage greater consistency in how private banks operating in Luxembourg approach securities-backed lending.

The CSSF’s intervention also reflects a wider regulatory trend towards more consistent application of EU prudential rules and reduced scope for bespoke interpretation.

For advisers, banks and insurers alike, it underlines the importance of monitoring regulatory developments at the intersection of lending, insurance and cross-border planning.

Brendan Harper

Head of Asia and HNW Technical Services

Des échanges récents de la part du régulateur financier luxembourgeois, la Commission de Surveillance du Secteur Financier (CSSF), ont remis en lumière la manière dont les banques doivent traiter, aux fins du capital réglementaire, les prêts adossés à des titres garantis par des contrats d’assurance-vie.

Dans cet article, Brendan Harper examine une clarification réglementaire qui, bien que technique, a des implications pratiques pour les banques, les conseillers et les clients, en particulier dans un contexte où les notations de crédit des assureurs jouent un rôle de plus en plus central dans les décisions de financement.

Les financements adossés à des titres continuent de jouer un rôle important dans la banque privée, permettant aux clients de générer de la liquidité tout en conservant des structures d’investissement ou de planification à long terme. Au Luxembourg, cela implique fréquemment qu’un contrat d’assurance-vie soit nanti ou cédé à une banque en garantie du prêt.

Dans le cadre du règlement européen sur les exigences de fonds propres (CRR - Capital Requirements Regulation), les banques doivent calculer un montant d’exposition pondéré par les risques pour ce type de financement. Celui-ci détermine le niveau de capital réglementaire que la banque doit détenir et influence directement l’appétit pour le crédit, la tarification et l’économie globale du prêt.

Les échanges récents avec la CSSF se sont concentrés sur la manière dont ces règles doivent être appliquées lorsque des contrats d’assurance-vie sont utilisés comme garantie.

Bien que la correspondance de la CSSF n’ait pas été rendue publique, son contenu a été confirmé auprès des acteurs du marché et des conseillers. Le régulateur a rappelé à certaines banques privées la bonne application de l’article 232 du CRR lorsque des contrats d’assurance-vie sont donnés en garantie.

La CSSF a remis en question les pratiques consistant à adopter une approche de « look-through » sur les actifs sous-jacents détenus dans le contrat lors de l’évaluation du risque de crédit. L’article 232 prévoit au contraire que les banques substituent le risque de crédit de l’emprunteur par celui de l’organisme d’assurance émettant le contrat.

En pratique, cela signifie que le risque pertinent est la qualité de crédit de l’assureur, et non son ratio de solvabilité ni la composition des actifs d’investissement sous-jacents au contrat.

Cela reflète une réalité juridique et réglementaire. En cas d’insolvabilité de l’assureur, les banques ne disposent pas de droits directs sur les actifs de celui-ci. L’analyse réglementaire se concentre donc sur la solidité financière et la qualité de crédit de l’assureur en tant que contrepartie.

Une conséquence clé de cette approche est l’importance croissante des notations de crédit indépendantes des assureurs.

Dans le cadre du CRR :

À l’inverse, les assureurs ne disposant pas de notation de crédit indépendante peuvent être classés dans des catégories de risque plus élevées. Cela peut entraîner des exigences en capital plus importantes et des conditions de financement moins compétitives.

D’un point de vue réglementaire, la clarification apportée par la CSSF confirme que les notations de crédit ne constituent pas uniquement un élément de communication. Elles représentent un facteur pertinent dans la manière dont les banques évaluent, structurent et tarifient les financements adossés à des titres.

Pour les conseillers accompagnant des clients fortunés ou internationalement mobiles, cette évolution rappelle que les décisions de structuration peuvent avoir des conséquences en aval sur les conditions de financement bancaire.

Lorsque l’assurance‑vie est utilisée pour soutenir un financement adossé à des titres :

Il ne s’agit pas d’une évolution du cadre juridique, mais d’une clarification des attentes des autorités de supervision. À terme, cela pourrait conduire à une plus grande cohérence dans la manière dont les banques privées opérant au Luxembourg abordent les prêts sur titres.

L’intervention de la CSSF reflète également une tendance réglementaire plus large visant à assurer une application plus cohérente des règles prudentielles européennes et à limiter les marges d’interprétation spécifiques.

Pour les conseillers, les banques et les assureurs, cela souligne l’importance de suivre les évolutions réglementaires à l’intersection du financement, de l’assurance et de la planification transfrontalière.

Simon Martin

Head of UK Technical Services

From 18 May 2026, tax advisers who are paid to interact with HM Revenue and Customs (HMRC) on behalf of clients will be required to register with HMRC and meet minimum professional standards.

HMRC has indicated that the new register will strengthen its ability to monitor adviser behaviour and exclude those who fail to meet required standards, forming part of a wider effort to raise standards in the tax advice market.

The definition of a tax adviser is intentionally broad. It covers:

Any person or organisation who, in the course of a business, assists other persons with their tax affairs.

For these purposes, assisting a person with their tax affairs includes any of the following activities:

A person may still fall within the definition of a tax adviser even if:

The registration requirement also applies to firms and individuals based overseas where they interact with HMRC.

A person or organisation meeting the definition of a tax adviser must not interact with HMRC unless registered.

The registration obligation applies to the legal entity that interacts with HMRC. Individual employees will not need to register separately, although firms must provide details of relevant individuals as part of the process. Registration will take place through an online system, which is currently under development.

For these purposes, interacting with HMRC includes:

Tax advisers who do not hold an Agent Services Account (ASA) will generally be required to register from 18 May 2026, although deadlines may vary depending on the nature of the activity. At the time of writing, the deadline for overseas tax advisers has not yet been confirmed.

Failure to register may result in a compliance notice being issued. Continued interaction with HMRC after a compliance notice has been served can lead to financial penalties, which may apply to the firm and/or the individual.

Certain activities and individuals are exempt from the registration requirement. These include, but are not limited to:

Although the draft Finance Bill legislation does not require advisers to be members of a professional body, registration is conditional on meeting defined standards.These include confirmation that the adviser:

In addition, advisers must:

Advisers should consider whether their activities involve interaction with HMRC that will trigger the new registration requirement. Early review is advisable, particularly where services are provided across borders or through complex structures.

Failure to register, or to meet the required standards, may result in financial penalties and restrictions on future dealings with HMRC.

Further guidance is available from professional bodies, including the Association of Tax Technicians (ATT) and the Chartered Institute of Taxation (CIOT).

The current draft legislation can be accessed here:

https://www.gov.uk/government/publications/modernising-and-mandating-tax-adviser-registration-with-hmrc/draft-legislation-accessible-version

This quarter’s Technical Spotlight explores why life insurance sits at the centre of holistic wealth planning, using insights from France, Portugal, Sweden, Asia and the UK to show how a single, adaptable structure can bring coherence to complex cross-border plans.

Brendan Harper

Head of Asia and HNW Technical Services

Brendan Harper explores why life insurance is increasingly positioned at the heart of effective wealth planning for high-net-worth families.

Drawing on insights from multiple markets, he explains how insurance-based wealth solutions can bring structure, portability and coherence to complex, cross-border wealth strategies.

Nicolas Morhun

Senior Wealth Planner, Associate Director – France

Alexandra Habermann

Wealth Planner - France

Mafalda Moura Cesário

Head of Tax and Legal – Portugal/Brazil

Roberth Josefsson

Senior Wealth Planner – Sweden

Peter Tung

Tax and Legal Counsel – Asia

Lana Jarvis

Senior Wealth Planner – UK

Aidan Golden

Head of Group Technical Services

Stephen Atkinson

Global Head of Sales and Marketing, Utmost

As private market assets move from the margins into the core of high-net-worth portfolios, the structures used to hold them and the governance that supports those structures are coming under increasing scrutiny.

In this interview, Aidan Golden talks to Stephen Atkinson, Global Head of Sales and Marketing at Utmost, about how the expectations of regulatory authorities are evolving, what this means for advisers and trustees, and why good outcomes increasingly depend on how assets are administered, valued and funded over time, not just on what is being invested in.

Brendan Harper

Head of Asia and HNW Technical Services

Modern wealth planning for high-net-worth families is characterised by growing complexity. Clients often hold diverse asset types, lead cross-border lives and face evolving tax, regulatory and succession challenges over time. Against this backdrop, structures designed in isolation or with a single jurisdiction in mind frequently fail to deliver sustainable outcomes.

Life insurance increasingly sits at the centre of a holistic wealth planning strategy, acting as a unifying framework capable of addressing multiple planning needs through a single, adaptable structure. The supporting articles in this edition, drawn from several of Utmost’s core markets illustrate how this principle applies in practice across differing jurisdictions and client circumstances.

Across markets where Utmost is active, common planning needs continue to emerge. These include:

Few planning structures can address all these needs in a coordinated and efficient way. More commonly, they are tackled separately, resulting in fragmented planning and, often, unintended consequences.

Below I consider how such fragmentation can arise, and why an insurance-based wealth solution can often provide a more effective solution.

Liquidity is frequently sourced through borrowing against existing assets. However, loan-to-value ratios may be constrained where assets are held directly, particularly where portfolios include illiquid or complex investments. By contrast, restructuring assets into an insurance-based solution can facilitate higher levels of borrowing, as lenders are able to rely on the insurer’s credit rating when assessing capital requirements.

Family protection is often addressed separately through so-called high-net-worth insurance solutions, such as universal life or indexed universal life policies. These typically accept only cash premiums or very liquid assets and involve transferring capital to the insurer, resulting in a loss of investor control. From an asset manager’s perspective, this can also lead to a reduction in assets under management.

A variable universal life policy offers a more integrated approach. Existing investment mandates can often be retained, investment returns can be used to fund life cover, and private assets may also be incorporated. This allows protection to be embedded within the wider wealth strategy, preserving adviser and asset manager relationships while maintaining flexibility to adjust cover as client priorities change.

Planning structures are often designed with a client’s current jurisdiction in mind. Increasing international mobility means that purely local solutions can unravel when cross-border elements arise. This can result in exposure to anti-avoidance regimes, conflicts of law or additional tax and reporting obligations.

Life insurance, by its nature, operates across jurisdictions. This universality means family members who relocate are more likely to retain their interests in the structure without triggering adverse tax or legal consequences. It provides a level of continuity that many domestic structures struggle to achieve.

Life insurance facilitates wealth transfer through contractual beneficiary nomination mechanisms. In many jurisdictions, these are recognised in law and may create a separate estate for succession purposes. This allows wealth to pass efficiently and without delay, often avoiding probate and reducing the need for complex succession structures that require clients to relinquish day-to-day control.

Additional benefits can include creditor protection, mitigation of forced heirship rules and, in certain circumstances, reduced inheritance tax exposure.

The transfer of assets into complex trust or corporate structures does not always produce favourable tax outcomes, particularly where high-tax jurisdictions are involved. On the contrary, such structures may attract targeted anti-avoidance provisions and impose significant compliance burdens.

Life insurance typically operates within its own tax regime, allowing for tax-deferred growth and, in many cases, favourable tax treatment on surrender or death. This can deliver a more predictable and administratively efficient outcome for internationally mobile families.

Insurance policies can often be adapted by amending policy terms to reflect changes in residency, family circumstances or tax law. This level of flexibility is rarely available within irrevocable trusts or rigid corporate structures, which may be difficult or impossible to restructure once established.

Case Study Insights

Read the case study, How Planning in Isolation Can Quickly Unravel – a high-net-worth individual wants succession certainty in Dubai while retaining control, but his structure begins to unravel when he later relocates to Portugal and his tax position changes, highlighting the need for an integrated, portable framework.

Visit the Case Study Insights section below, or click here.

Brendan Harper

Head of Asia and HNW Technical Services

Brendan Harper analyse pourquoi l’assurance-vie est de plus en plus positionnée au cœur d’une planification patrimoniale efficace pour les familles fortunées.

S’appuyant sur des observations issues de différents marchés, il explique comment les solutions patrimoniales basées sur l’assurance peuvent apporter structure, portabilité et cohérence à des stratégies patrimoniales internationales complexes.

La planification patrimoniale moderne des clients fortunés se caractérise par une complexité croissante. Les clients détiennent souvent des actifs diversifiés, mènent des vies transfrontalières et sont confrontés à des enjeux évolutifs en matière de fiscalité, de réglementation et de transmission au fil du temps. Dans ce contexte, les structures conçues de manière isolée ou en fonction d’une seule juridiction ne permettent souvent pas d’atteindre des résultats durables.

L’assurance-vie occupe de plus en plus une place centrale dans une stratégie globale de planification patrimoniale, en agissant comme un cadre structurant capable de répondre à de multiples besoins de planification au sein d’une structure unique et adaptable. Les articles associés dans cette édition, issus de plusieurs marchés clés d’Utmost, illustrent la manière dont ce principe s’applique concrètement dans différentes juridictions et selon les situations des clients.

Sur les marchés où Utmost est présent, des besoins de planification communs continuent d’émerger. Ceux-ci incluent :

Peu de structures de planification permettent de répondre à l’ensemble de ces besoins de manière coordonnée et efficace. Le plus souvent, ils sont traités séparément, ce qui conduit à une planification fragmentée et, fréquemment, à des conséquences non souhaitées.

Les sections ci-dessous examinent comment cette fragmentation peut apparaître et pourquoi une solution patrimoniale basée sur l’assurance peut souvent offrir une réponse plus efficace.

La liquidité est souvent obtenue par le biais d’un financement adossé aux actifs existants. Toutefois, les ratios de prêt peuvent être limités lorsque les actifs sont détenus en direct, en particulier lorsque les portefeuilles incluent des investissements illiquides ou complexes. À l’inverse, la restructuration des actifs au sein d’une solution basée sur l’assurance peut permettre des niveaux d’endettement plus élevés, les prêteurs pouvant s’appuyer sur la notation de crédit de l’assureur pour évaluer leurs exigences en capital.

La protection de la famille est souvent traitée séparément au moyen de solutions dites d’assurance pour clients fortunés, telles que les contrats universal life ou indexed universal life. Ces solutions n’acceptent généralement que des primes en numéraire ou des actifs très liquides et impliquent un transfert de capital à l’assureur, entraînant une perte de contrôle pour l’investisseur. Du point de vue du gestionnaire d’actifs, cela peut également conduire à une diminution des actifs sous gestion.

Un contrat de type variable universal life offre une approche plus intégrée. Les mandats d’investissement existants peuvent souvent être conservés, les rendements peuvent être utilisés pour financer la couverture, et des actifs privés peuvent également être intégrés. Cela permet d’intégrer la protection au sein de la stratégie patrimoniale globale, tout en préservant les relations avec les conseillers et les gestionnaires d’actifs et en maintenant la flexibilité nécessaire pour ajuster la couverture en fonction de l’évolution des priorités du client.

Les structures de planification sont souvent conçues en fonction de la juridiction actuelle du client. L’augmentation de la mobilité internationale signifie que les solutions purement locales peuvent se fragiliser lorsque des éléments transfrontaliers apparaissent. Cela peut entraîner une exposition à des dispositifs anti-abus, des conflits de lois ou des obligations fiscales et déclaratives supplémentaires.

L’assurance-vie, par nature, s’inscrit dans un cadre international. Cette universalité signifie que les membres de la famille qui changent de résidence sont plus susceptibles de conserver leurs droits dans la structure sans déclencher de conséquences fiscales ou juridiques défavorables. Elle offre un niveau de continuité que de nombreuses structures domestiques peinent à atteindre.

L’assurance-vie permet la transmission du patrimoine grâce à des mécanismes contractuels de désignation de bénéficiaires. Dans de nombreuses juridictions, ces mécanismes sont reconnus en droit et peuvent constituer une masse distincte à des fins successorales. Cela permet une transmission efficace et sans délai, souvent en évitant les procédures successorales et en réduisant le recours à des structures complexes nécessitant un abandon du contrôle au quotidien par le client.

Parmi les avantages complémentaires peuvent figurer la protection contre les créanciers, l’atténuation des règles de réserve héréditaire et, dans certaines situations, une réduction de l’exposition aux droits de succession.

Le transfert d’actifs dans des structures complexes de type trust ou sociétés ne produit pas toujours des résultats fiscaux favorables, en particulier dans les juridictions à forte fiscalité. Au contraire, ces structures peuvent être visées par des dispositifs anti-abus spécifiques et générer des obligations déclaratives importantes.

L’assurance-vie fonctionne généralement dans un cadre fiscal propre, permettant une capitalisation avec différé d’imposition et, dans de nombreux cas, un traitement fiscal favorable lors du rachat ou du décès. Cela peut offrir un résultat plus prévisible et plus efficient sur le plan administratif pour les familles internationales.

Les contrats d’assurance peuvent souvent être adaptés par modification des conditions contractuelles afin de refléter les changements de résidence, de situation familiale ou de cadre fiscal. Ce niveau de flexibilité est rarement disponible dans des structures irrévocables telles que les trusts ou certaines structures sociétaires, qui peuvent être difficiles, voire impossibles, à restructurer une fois mises en place.

Étude de cas

Lisez l’étude de cas Comment une planification menée de manière isolée peut rapidement se fragiliser – une personne fortunée souhaite sécuriser sa transmission à Dubaï tout en conservant le contrôle, mais sa structure commence à se fragiliser lorsqu’elle s’installe ultérieurement au Portugal et que sa situation fiscale évolue, mettant en évidence la nécessité d’un cadre intégré et portable.

Consultez la section Étude de cas ci-dessous ou cliquez ici.

Nicolas Morhun

Senior Wealth Planner, Associate Director – France

Alexandra Habermann

Wealth Planner - France

In France, wealth planning is often approached through a combination of tax optimisation, civil law structuring and investment management. When these elements are addressed separately, however, the result can be fragmented planning that exposes families to rigidity, inefficiency and unintended consequences over time.

Within this context, the life insurance contract has evolved into a central planning framework capable of addressing several core planning needs through a single, coherent structure. While the tax advantages of French life insurance are well understood, its civil law characteristics and financial flexibility are equally important in explaining its enduring success as a holistic wealth planning tool.

Life insurance offers several well-established tax advantages. When used as part of a broader planning strategy, these benefits can contribute not only to income tax efficiency but also to the management of wider tax exposure.

Tax Treatment During the Lifetime of the Contract

During its lifetime, a life insurance contract offers several favourable tax features, including:

While these advantages are significant, their effectiveness is maximised when aligned with succession planning and asset protection objectives. Designing tax solutions in isolation can lead to structures that are difficult to adapt or inefficient when wider planning considerations are taken into account.

Tax Treatment on Death

The tax treatment of capital paid to beneficiaries depends on the policyholder’s age when premiums were paid and on the timing of those payments.

Used appropriately, life insurance therefore enables optimisation not only of tax rates but also of taxable values.

Although tax considerations often drive the initial use of life insurance in France, its civil law features play a central role in supporting holistic planning outcomes.

Protection From Seizure

A life insurance contract is, by nature, protected from seizure by the policyholder’s creditors, provided the structure is implemented proactively and not in anticipation of financial difficulty. This protection is subject to limited exceptions, including:

When used correctly, this feature contributes to the robustness of the planning structure.

Freedom of Beneficiary Designation

Life insurance offers significant flexibility in drafting and amending beneficiary clauses throughout the lifetime of the contract. This allows policyholders to adapt their succession planning over time without the cost or rigidity often associated with alternative structures.

Importantly, the value of the policy is transferred outside the deceased’s estate and is not subject to forced heirship rules. This enables a degree of freedom of disposal that is difficult to achieve using traditional estate planning tools alone.

Beyond tax and civil law considerations, financial flexibility is a key factor in the enduring relevance of life insurance as a planning tool. Luxembourg and Irish insurers offer a wide range of investment options, including discretionary and advisory mandates.

During the lifetime of the contract, investment strategies can be adjusted, supplemented or replaced without triggering a taxable event, provided investments remain within the insurer’s acceptance policy. This allows the structure to evolve alongside the policyholder’s circumstances, objectives and level of investment sophistication.

French life insurance remains a core pillar of holistic wealth planning, not only for its tax advantages, but for its ability to integrate tax, civil law and financial objectives within a single, adaptable structure.

To ensure solutions are aligned with client objectives and the French legal and regulatory framework, advisers should engage with their Utmost sales representative for further guidance and support when structuring life insurance arrangements.

Nicolas Morhun

Senior Wealth Planner, Associate Director

Alexandra Habermann

Wealth Planner

En France, la planification patrimoniale repose souvent sur une combinaison prenant en compte les aspects fiscaux, civils et de gestion financière. Lorsque ces trois aspects sont traités séparément, il en résulte fréquemment une approche fragmentée, exposant les familles à des rigidités, des inefficiences et des conséquences non anticipées dans le temps.

Dans ce contexte, le contrat d’assurance vie s’est imposé comme une solution offrant un cadre central de planification, capable de répondre à plusieurs besoins fondamentaux au sein d’une structure unique et cohérente. Si les avantages fiscaux de l’assurance vie française sont largement connus et n’ont plus besoin d’être démontrés, ses caractéristiques en droit civil et sa flexibilité financière sont tout aussi déterminantes pour expliquer son succès durable en tant qu’outil de planification patrimoniale holistique.

L’assurance vie offre plusieurs avantages fiscaux bien déterminés. Lorsqu’elle s’inscrit dans une stratégie patrimoniale globale, elle contribue non seulement à l’efficience fiscale en matière d’impôt sur le revenu, mais également à la gestion d’une exposition fiscale plus large.

Traitement fiscal pendant la durée du contrat

Durant la vie du contrat, l’assurance vie présente de nombreux avantages fiscaux parmi lesquels :

Si ces avantages sont significatifs, leur efficacité est maximale lorsqu’ils sont alignés avec des objectifs de transmission et de protection du patrimoine. Concevoir une solution fiscale isolée peut conduire à des structures difficiles à faire évoluer ou inefficaces lorsque les autres aspects de la planification patrimoniale ne sont pas prises en compte.

Traitement fiscal en cas de décès

La fiscalité applicable aux capitaux décès versés aux bénéficiaires, dépend de l’âge du souscripteur au moment du versement des primes, ainsi que de la date à laquelle ces versements ont été effectués.

Utilisée de manière appropriée, l’assurance vie permet ainsi d’optimiser non seulement les taux d’imposition, mais également la base taxable.

Si les considérations fiscales sont souvent la motivation principale au recours à l’assurance vie en France, ses caractéristiques en droit civil jouent un rôle central dans la la mise en place d’une planification patrimoniale globale optimisée.

Protection contre les saisies

Par principe, le contrat d’assurance vie est protégé contre les poursuites des créanciers du souscripteur, à condition que sa mise en place intervienne de manière anticipée et non dans un contexte de difficultés financières. Ce principe connaît toutefois certaines exceptions, notamment en cas de :

Bien utilisé, cette protection renforce la solidité de la structuration patrimoniale.

Liberté de désignation des bénéficiaires

L’assurance vie offre une grande souplesse quant à la rédaction et la modification de la clause bénéficiaire tout au long de la vie du contrat. Elle permet ainsi d’adapter la transmission du patrimoine au fil du temps, sans supporter ni les coûts, ni les rigidités souvent associés à d’autres solutions patrimoniales.

Il est essentiel de souligner que les capitaux d’assurance vie sont transmis hors succession et ne sont pas soumis aux règles de la réserve héréditaire. Cette caractéristique confère une liberté de disposition difficile à obtenir par les seuls outils successoraux traditionnels.

Au delà des considérations fiscales et civiles, la flexibilité financière constitue un facteur clé de la pertinence de l’assurance vie comme outil de planification patrimoniale. Les assureurs luxembourgeois et irlandais proposent une large palette de solutions d’investissement, incluant des mandats discrétionnaires ou conseillés.

En cours de vie du contrat, les stratégies d’investissement peuvent être ajustées, complétées ou remplacées sans être un fait générateur d’impôt, sous réserve que les supports retenus respectent la politique d’acceptation de l’assureur. Cette souplesse permet à la structure de suivre l’évolution de la situation personnelle du souscripteur, de ses objectifs et de son niveau de sophistication patrimoniale.

L’assurance vie française demeure un pilier central de la planification patrimoniale holistique, non seulement en raison de ses avantages fiscaux, mais aussi en raison de la possibilité qu’elle offred’intégrer des objectifs fiscaux, civils et financiers au sein d’une structure unique et évolutive.

Afin de s’assurer que les solutions mises en place sont pleinement alignées avec les objectifs des clients et avec le cadre juridique et réglementaire français, il est recommandé aux conseillers d’échanger avec leur représentant commercial Utmost pour bénéficier d’un accompagnement personnalisé et de conseils sur-mesure adaptés lors de la structuration des contrats d’assurance vie.

Mafalda Moura Cesário

Head of Tax and Legal – Portugal/Brazil

Portugal has long attracted internationally mobile individuals, entrepreneurs and retirees seeking a stable environment in which to live, invest and plan for the future. As client profiles have become more international and asset bases more diverse, the need for cohesive, forward-looking wealth planning has increased significantly.

In this context, unit-linked life insurance policies have evolved into a valuable holistic planning framework. They can bring together investment, protection and estate planning objectives within a single structure. This is particularly relevant in Portugal’s post-NHR environment, where planning decisions increasingly need to account for long-term flexibility, cross-border considerations and regulatory change.

Unit-linked life insurance policies combine two core elements of wealth planning: investment and protection. Unlike traditional insurance contracts offering fixed or predefined returns, unit-linked policies are linked to underlying investments, allowing policy values to rise or fall in line with asset performance.

This hybrid structure enables advisers to address multiple objectives within a single policy, including:

By addressing these objectives together rather than in isolation, unit-linked policies can help reduce the fragmentation that often arises when portfolios are spread across multiple, disconnected structures.

One reason unit-linked policies continue to play an important role in Portugal is their tax efficiency when used as part of a long-term strategy.

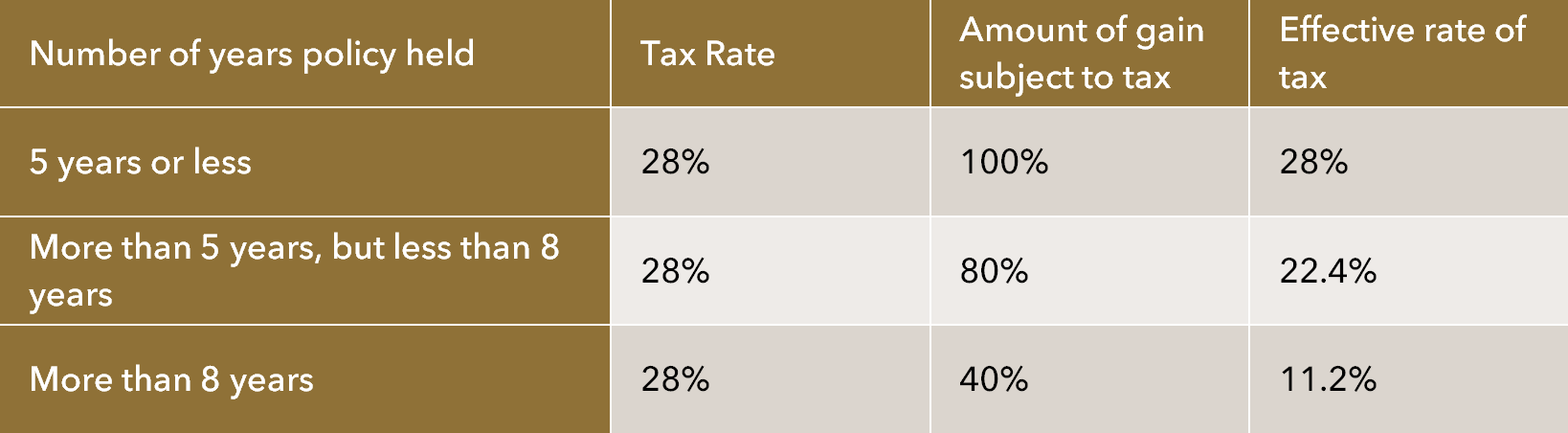

Investment gains generated within the policy are not taxed until surrender. This allows policyholders to benefit from tax deferral and encourages a more disciplined investment approach. Portugal also rewards long-term holding periods. Depending on the duration of the policy and the structure of premium payments, the effective tax rate on the income element of a surrender can reduce significantly after eight years to 11.2%.

Illustrative example:

If a client realises €100,000 of taxable income on a surrender after eight years of holding the policy, tax at 11.2% would be €11,200. At the standard 28% rate, the tax would be €28,000. The long-term holding therefore results in a tax saving of €16,800 on the gain element alone.

For individuals focused on long-term wealth accumulation rather than short-term market movements, this feature provides both tax efficiency and behavioural discipline.

Portugal’s wealth planning landscape has shifted following the replacement of the original Non-Habitual Resident (NHR) regime with the more targeted NHR 2.0 framework.

While NHR 2.0 remains attractive, its narrower scope requires internationally mobile individuals to adopt more structured and forward-looking planning solutions. In this environment, unit-linked life insurance policies can provide a practical way to organise investment assets within a single framework that remains adaptable as tax and regulatory conditions evolve.

Under NHR 2.0, qualifying individuals may benefit from favourable treatment on specific categories of foreign-source income, subject to the detailed conditions of the regime. Where a unit-linked policy is issued by a non-Portuguese insurer, qualifying policyholders may also benefit from tax-exempt surrenders, aligning long-term tax efficiency with portability.

By contrast, income sourced from jurisdictions included on Portugal’s blacklisted jurisdictions can be subject to an aggravated tax rate of 35%, rather than the standard 28% applicable to certain categories of capital income. These so-called blacklisted jurisdictions include, for example, the Cayman Islands, British Virgin Islands and Panama, among others.

For advisers, this distinction is critical. Where client portfolios include exposure to assets or structures linked to blacklisted jurisdictions, insurance-based structuring can play an important role in managing both tax exposure and compliance complexity within the post-NHR framework.

Using a unit-linked policy as an umbrella therefore remains a valuable structuring approach, particularly for internationally mobile clients navigating a more targeted and technically demanding regime.

Beyond investment considerations, unit-linked life insurance plays a central role in succession planning for families resident in, or connected to, Portugal.

Death benefits are typically paid directly to designated beneficiaries rather than passing through the deceased’s estate. This can simplify inheritance planning, improve liquidity on death and reduce administrative complexity, particularly for internationally mobile families with assets and heirs in multiple jurisdictions.

Crucially, life insurance can also support post-mortem control. Death benefit settlement can be structured to allow for deferred or controlled distribution, rather than a single lump-sum payment. This enables advisers to align the timing and manner of payment with family governance objectives, beneficiary maturity and cross-border considerations.

For families with younger beneficiaries, blended family dynamics or significant international exposure, this ability to manage how and when wealth is transferred can be as important as who ultimately receives it. In this way, life insurance allows succession planning to be integrated into the broader wealth structure, rather than treated as a one-off event.

A core principle of holistic wealth planning is adaptability. Personal circumstances, family structures, tax rules and investment objectives inevitably evolve over time.

Unit-linked policies offer a high degree of flexibility. Policyholders can adjust investment allocations, switch funds and update beneficiary designations as circumstances change. Provided investments remain within the insurer’s acceptance policy, these adjustments can usually be made without triggering a taxable event.

This ability to evolve over time distinguishes life insurance from more rigid planning structures, which may be difficult or costly to amend once established.

As wealth planning becomes more interconnected, demand for integrated, long-term solutions continues to grow. In Portugal’s evolving tax and regulatory landscape, unit-linked life insurance policies provide a practical way to align investment growth, tax efficiency, succession planning and flexibility within a single framework.

Rather than functioning solely as an investment or tax tool, life insurance is increasingly positioned as a cornerstone of holistic wealth planning for Portuguese residents and internationally mobile individuals alike.

Further reading on NHR 2.0

For a practical overview of eligibility, key deadlines and planning points for advisers. Read this article from Navigator Winter 2026:

Portugal: Understanding the New Inpatriate Regime (NIR) After the End of NHR

Mafalda Moura Cesário

Head of Tax and Legal – Portugal/Brasil

Portugal tem atraído, há vários anos, indivíduos com mobilidade internacional, empresários e reformados que procuram um ambiente estável para viver, investir e planear o futuro. Com a internacionalização do perfil dos clientes e a diversificação dos seus ativos, a necessidade de um planeamento patrimonial coeso e voltado para o futuro aumentou significativamente.

Neste contexto, as apólices de seguro de vida unit linked evoluíram para uma estrutura de planeamento holístico valiosa. Permitem integrar objetivos de investimento, proteção e planeamento sucessório numa única estrutura. Esta abordagem é particularmente relevante no contexto pós RNH em Portugal, onde as decisões de planeamento exigem cada vez mais flexibilidade a longo prazo, atenção às questões transfronteiriças e adaptação à evolução regulamentar.

As apólices de seguro de vida unit linked combinam dois elementos fundamentais do planeamento patrimonial: investimento e proteção. Ao contrário dos contratos de seguro tradicionais, que oferecem rendimentos fixos ou predefinidos, as apólices unit linked estão ligadas a investimentos subjacentes, permitindo que o valor da apólice evolua em função do desempenho dos ativos.

Esta estrutura híbrida permite aos consultores abordar vários objetivos num único contrato, incluindo:

Ao tratar estes objetivos de forma integrada, em vez de isolada, as apólices unit linked ajudam a reduzir a fragmentação que frequentemente resulta da dispersão do património por várias estruturas desconexas.

Uma das razões pelas quais as apólices unit linked continuam a desempenhar um papel relevante em Portugal é a sua eficiência fiscal quando integradas numa estratégia de longo prazo.

Os rendimentos gerados no seio da apólice não são tributados até ao momento do resgate. Isto permite aos investidores beneficiar de um diferimento da tributação e favorece uma abordagem de investimento mais disciplinada.

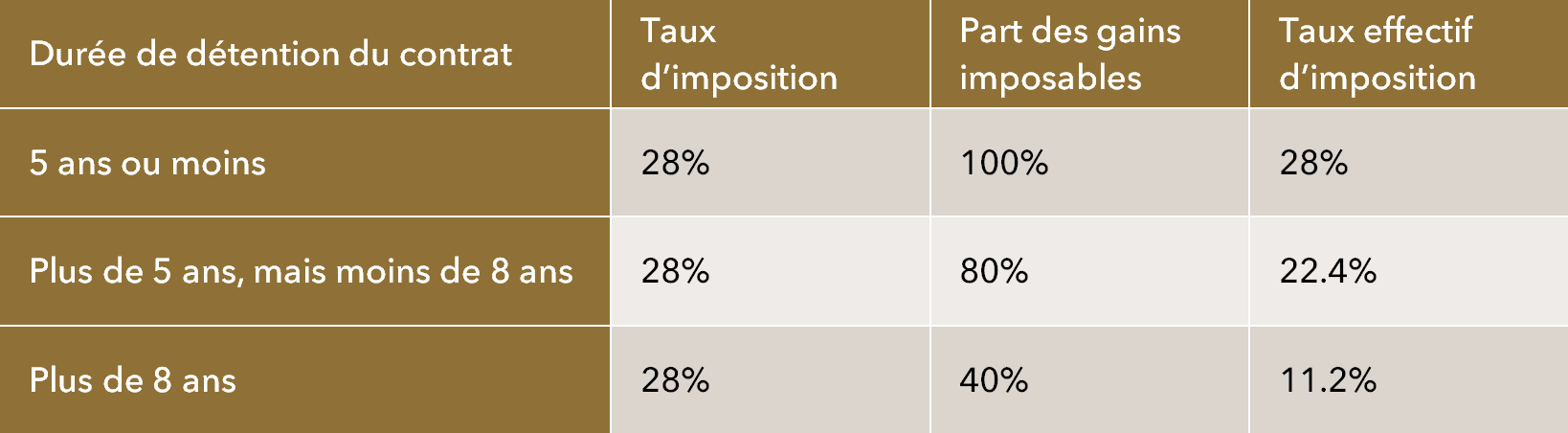

Portugal também premeia períodos de investimento de longo prazo. Dependendo da duração da apólice e da estrutura de pagamento dos prémios, a taxa efetiva de imposto sobre o rendimento resultante de um resgate pode reduzir significativamente para 11,2% após oito anos.

Exemplo ilustrativo:

Se um cliente obtiver um ganho de rendimento tributável de € 100.000 com o resgate de uma apólice após oito anos de detenção da apólice, o imposto correspondente a 11,2% seria de € 11.200. À taxa não reduzida de 28%, o imposto seria de € 28.000. Portanto, no longo prazo, somente no elemento do ganho, a detenção da apólice resulta numa poupança fiscal de € 16.800.

Para investidores focados na acumulação patrimonial de longo prazo, e não em movimentos de curto prazo do mercado, esta característica oferece simultaneamente eficiência fiscal e disciplina comportamental.

O enquadramento do planeamento patrimonial em Portugal sofreu alterações significativas com a substituição do regime original dos Residentes Não Habituais (RNH) pelo regime RNH 2.0.

Embora o regime dos NHR 2.0 continue a ser atrativo, o seu âmbito mais restrito exige que os indivíduos internacionalmente móveis adotem soluções de planeamento mais estruturadas e prospetivas. Neste contexto, as apólices de seguro unit linked podem oferecer uma forma descomplicada de organizar ativos de investimento numa estrutura única que permanece adaptável à medida que as condições tributárias e regulatórias evoluem.

Ao abrigo dos RNH 2.0, os indivíduos elegíveis podem beneficiar de um tratamento favorável em categorias específicas de rendimentos de origem estrangeira, sujeitos às condições especificadas no regime. Quando uma apólice de seguro de vida com componente de investimento é emitida por uma seguradora não portuguesa, os tomadores de apólices elegíveis podem também beneficiar de resgates isentos de impostos, alinhando a eficiência fiscal a longo prazo com a portabilidade.

Em contrapartida, os rendimentos provenientes de jurisdições incluídas na lista de paraísos fiscais, que englobam territórios com "regimes fiscais claramente mais favoráveis", podem estar sujeitos a uma taxa de imposto agravada de 35%, em vez dos 28% aplicáveis a determinadas categorias de rendimentos de capital.

Estes paraísos fiscais incluem, por exemplo, as Ilhas Caimão, as Ilhas Virgens Britânicas e o Panamá, entre outras.

Para os consultores, esta distinção é crucial. Quando as carteiras dos clientes incluem exposição a ativos ou estruturas ligadas a jurisdições constante da lista de paraísos fiscais, a estruturação baseada em seguros pode desempenhar um papel importante na gestão da exposição fiscal e da complexidade do cumprimento das normas no âmbito do regime pós-RNH.

Utilizar uma apólice de seguro de vida unit-linked como proteção continua, portanto, a ser uma abordagem de estruturação valiosa, especialmente para clientes com mobilidade internacional que operam num regime mais direcionado e tecnicamente exigente.

Para além das considerações de investimento, o seguro de vida unit linked desempenha um papel importante no planeamento sucessório de famílias residentes em Portugal ou com ligações ao país.

As prestações por morte são, em regra, pagas diretamente aos beneficiários designados, sem integrarem a habelitação de herdeiros do falecido. Este mecanismo pode simplificar o planeamento sucessório, melhorar a liquidez no momento do óbito e reduzir a complexidade administrativa, especialmente para famílias internacionalmente móveis com ativos e herdeiros em várias jurisdições.

Fundamentalmente, o seguro de vida também pode auxiliar no controle pós-morte. O pagamento do benefício por morte pode ser estruturado para permitir a distribuição diferida ou controlada, em vez de um pagamento único. Isso permite que os consultores alinhem o momento e a forma de pagamento com os objetivos de gestão familiar, a maturidade do beneficiário e as considerações internacionais.

Para famílias com beneficiários mais jovens, dinâmicas familiares complexas ou significativa exposição internacional, a capacidade de gerir como e quando o património é transferido pode ser tão importante quanto quem o recebe em última instância. Dessa forma, o seguro de vida permite que o planeamento sucessório seja integrado na estrutura patrimonial mais ampla, em vez de ser tratado como um evento isolado.

Um princípio essencial do planeamento patrimonial holístico é a adaptabilidade. As circunstâncias pessoais, as estruturas familiares, as regras fiscais e os objetivos de investimento evoluem inevitavelmente ao longo do tempo.

As apólices unit linked oferecem um elevado grau de flexibilidade. Os titulares podem ajustar a alocação de investimentos, efetuar trocas entre fundos e atualizar as designações de beneficiários à medida que as suas circunstâncias mudam. Desde que os investimentos permaneçam dentro da política de aceitação da seguradora, estas alterações podem, regra geral, ser realizadas sem desencadear um evento tributável.

Esta capacidade de adaptação distingue o seguro de vida de estruturas mais rígidas, que podem ser difíceis ou dispendiosas de alterar após a sua constituição.

À medida que o planeamento patrimonial se torna cada vez mais integrado, a procura por soluções de longo prazo e abrangentes continua a crescer. No contexto fiscal e regulamentar em evolução em Portugal, as apólices de seguro de vida unit linked oferecem uma forma prática de alinhar o crescimento do investimento, eficiência fiscal, planeamento sucessório e flexibilidade num único enquadramento.

Em vez de funcionar apenas como um instrumento de investimento ou fiscal, o seguro de vida é cada vez mais assumido como um pilar central do planeamento patrimonial holístico, tanto para residentes em Portugal como para indivíduos internacionalmente móveis.

Roberth Josefsson

Senior Wealth Planner – Sweden

Swedes are a highly mobile population, moving abroad and returning to Sweden more frequently than many of their Nordic neighbours. While international mobility offers lifestyle and professional opportunities, it also introduces complexity across banking, investments, taxation and succession planning.

In this context, insurance-based solutions increasingly serve as a central planning framework, allowing advisers to manage cross-border investment, tax and succession considerations within a single, coherent structure. When planning is approached in a fragmented way, clients may be exposed to unintended tax consequences, compliance failures and unnecessary complexity.

Many Swedish residents already hold domestic life insurance policies or investment savings accounts (ISK accounts), which benefit from Sweden’s preferential yield tax regime. A common misconception is that these vehicles retain their tax and regulatory characteristics when clients relocate abroad. In practice, this is rarely the case.

The criteria for qualifying as a life insurance policy vary significantly between jurisdictions. A Swedish ISK account, for example, is typically treated as an ordinary bank account in other countries. This can result in exposure to local capital income and gains tax while continuing to attract Swedish yield tax, creating a risk of effective double taxation.

To support a successful relocation, planning should therefore take place before the move occurs. Swedish rules allow for the full surrender of a life insurance policy or withdrawal from an ISK account without Swedish taxation, creating an opportunity to restructure wealth in advance. Attempting to adapt an existing contract after relocation is often either not possible or sub-optimal.

Although Sweden does not levy inheritance or gift tax, clients relocating abroad are likely to encounter such taxes in their new jurisdiction. Establishing a compliant life insurance policy tailored to local requirements can therefore provide a robust succession planning solution, often with significant tax advantages.

Delivering this successfully requires an insurer with cross-border capability, experience across multiple jurisdictions and the ability to structure compliant solutions internationally. In this way, life insurance can act as an umbrella structure, aligning investment management, tax efficiency and succession planning within a single framework.

Consider a Swedish family relocating to Spain. They hold a domestic Swedish life insurance policy and an ISK account. Spanish legislation imposes specific requirements on life insurance contracts that Swedish policies typically do not meet. At the same time, the ISK account would be treated as an ordinary bank account, exposing the family to both Swedish and Spanish taxation.

By surrendering the Swedish arrangements before departure, without triggering Swedish tax, and establishing a locally compliant Spanish life insurance policy after relocation, the family may exit Sweden and enter Spain without immediate taxation. The Spanish policy can then help manage exposure to Spanish capital income tax, wealth tax and inheritance and gift tax, while also supporting structured succession planning.

International mobility does not end with relocation. Many Swedes later return home. Sweden’s abolition of net wealth, inheritance and gift taxes, combined with the option to apply yield tax rather than standard capital income tax, has enhanced the attractiveness of life insurance as an asset-holding structure.

Existing life insurance policies can often be brought back to Sweden without triggering taxation, provided they meet Swedish requirements, including a minimum uncapped life cover of 1%. Sweden also recognises beneficiary designations, reinforcing the role of life insurance as an effective succession planning tool on return.

Here again, pre-planning is essential to ensure the policy qualifies under Swedish rules before re-establishing residency.

For Swedish clients who move abroad and later return, an insurance-based wealth solution can provide continuity across jurisdictions. By anchoring planning within a flexible, internationally recognised structure, advisers can reduce fragmentation, manage tax exposure and support long-term succession objectives despite changing residency and regulatory environments.

Roberth Josefsson

Senior Wealth Planner – Sverige

Svenskar är en mycket mobil befolkning och flyttar utomlands – och återvänder till Sverige – oftare än många av sina nordiska grannar. Även om internationell rörlighet skapar livsstils och yrkesmässiga möjligheter, medför den också ökad komplexitet inom bank, investeringar, beskattning och successionsplanering.

I detta sammanhang fungerar försäkringsbaserade lösningar i allt högre grad som en central planeringsram. De gör det möjligt för rådgivare att hantera gränsöverskridande investerings , skatte och successionsfrågor inom en sammanhållen struktur. När planeringen sker på ett fragmenterat sätt riskerar kunder att drabbas av oavsiktliga skattekonsekvenser, bristande regelefterlevnad och onödig komplexitet.

Många svenska klienter har redan svenska livförsäkringar eller investeringssparkonton (ISK), som omfattas av den svenska schablonbeskattningen. En vanlig missuppfattning är att dessa lösningar behåller sina skattemässiga och regulatoriska egenskaper när klienten flyttar utomlands. I praktiken är detta sällan fallet.

Kriterierna för att ett avtal ska klassificeras som en livförsäkring varierar avsevärt mellan olika länder. Ett svenskt ISK konto behandlas till exempel normalt som ett vanligt bankkonto i andra jurisdiktioner. Detta kan leda till lokal beskattning av kapitalinkomster och kapitalvinster, samtidigt som schablonskatt fortsatt tas ut i Sverige – vilket skapar en risk för faktisk dubbelbeskattning.

För att en utflytt ska bli framgångsrik bör planeringen därför ske innan flytten äger rum. Enligt svenska regler är det möjligt att lösa in en livförsäkring eller ta ut medel från ett ISK utan svensk beskattning, vilket skapar ett tillfälle att omstrukturera tillgångarna i förväg. Att försöka anpassa befintliga lösningar efter utflyttning är ofta antingen inte möjligt eller mindre effektivt.

Även om Sverige inte tar ut arvsskatt eller gåvoskatt, kommer klienter som flyttar utomlands ofta i kontakt med sådana skatter i sitt nya hemland. Att etablera en lokalt anpassad och regelkonform livförsäkring kan därför utgöra en robust lösning för successionsplanering, ofta med betydande skattemässiga fördelar.

För att lyckas krävs ett försäkringsbolag med tydlig gränsöverskridande kapacitet, erfarenhet från flera jurisdiktioner och förmåga att strukturera internationellt regelefterlevande lösningar. På så sätt kan livförsäkringen fungera som en övergripande struktur där kapitalförvaltning, skatteeffektivitet och successionsplanering samordnas i ett och samma ramverk.

Föreställ dig en svensk familj som flyttar till Spanien. De har en svensk livförsäkring och ett ISK konto. Spansk lagstiftning ställer särskilda krav på livförsäkringar, vilka svenska försäkringar normalt inte uppfyller. Samtidigt behandlas ISK kontot som ett vanligt bankkonto, vilket kan leda till både svensk och spansk beskattning.

Genom att lösa in de svenska lösningarna före utflyttningen – utan att utlösa svensk skatt – och därefter etablera en lokalt anpassad spansk livförsäkring efter inflyttning, kan familjen lämna Sverige och etablera sig i Spanien utan omedelbar beskattning. Den spanska försäkringen kan därefter bidra till att hantera exponering mot spansk kapitalinkomstskatt, förmögenhetsskatt samt arv och gåvoskatt, samtidigt som den stödjer en strukturerad successionsplanering.

Internationell rörlighet tar inte slut vid utflyttning. Många svenskar återvänder senare till Sverige. Avskaffandet av förmögenhetsskatt, arvsskatt och gåvoskatt, i kombination med möjligheten att tillämpa schablonbeskattning i stället för traditionell kapitalinkomstskatt, har stärkt livförsäkringens attraktivitet som ägandeform för tillgångar.

Befintliga livförsäkringar kan ofta tas med tillbaka till Sverige utan att utlösa beskattning, förutsatt att de uppfyller svenska krav, inklusive ett minimalt obegränsat livförsäkringsskydd om 1 %. Sverige erkänner även förmånstagarförordnanden, vilket ytterligare förstärker livförsäkringens roll som ett effektivt verktyg för successionsplanering vid återflytt.

Även här är förhandsplanering avgörande, för att säkerställa att försäkringen kvalificerar enligt svenska regler innan bosättningen i Sverige återupptas.

För svenska klienter som flyttar utomlands och senare återvänder kan en försäkringsbaserad förmögenhetslösning skapa kontinuitet mellan olika länder. Genom att förankra planeringen i en flexibel och internationellt erkänd struktur kan rådgivare minska fragmentering, hantera skatteexponering och stödja långsiktiga successionsmål – trots förändrade bosättnings och regelverkssituationer.

Peter Tung

Tax and Legal Counsel – Asia

Asia’s private wealth continues to expand at an unprecedented pace. Driven by China, India and South-East Asia, total private wealth in the region is projected to reach USD 99 trillion by 2029 (BCG). At the same time, Asia is entering its largest intergenerational wealth transfer to date, with trillions expected to pass from founders to heirs, many of whom are internationally mobile and connected to multiple jurisdictions.

Despite this scale, succession and long-term planning remain underdeveloped in parts of the region. In China, for example, estate planning is still culturally unfamiliar. A Tsinghua University study of 67 listed-company founders who died between 2003 and 2024 found that only 9% left a will. High-profile inheritance disputes continue to highlight the risks that arise when wealth accumulates faster than it is structured.

Against this backdrop, life insurance is increasingly used as a central planning framework, allowing families to bring together liquidity management, succession planning and cross-border compliance within a single, coherent structure.

Across Asia, advisers are seeing a consistent set of factors prompting families to reassess existing arrangements:

In practice, advisers across Asia frequently encounter structures that have developed incrementally over time. These may combine family offices, operating companies and offshore trusts without meaningful integration.

The consequences can include:

In China, the consequences of fragmented succession planning are becoming increasingly visible. The Economist has observed that a new hereditary elite is emerging, even though formal estate planning remains relatively uncommon. Inheritance-related court judgments have risen sharply in recent years, driven by complex family structures and the absence of valid wills.

These developments reflect a broader regional dynamic. As wealth becomes more concentrated and asset structures more complex, fragmented arrangements struggle to deliver predictability, liquidity and continuity across generations. This reinforces the need for planning frameworks that provide clarity, governance and an orderly transfer of wealth over the long term.

Life insurance offers a balanced and defensible response to these challenges by providing a single structure capable of supporting multiple planning objectives.

Key features include:

While trusts and corporate entities continue to play an important role in governance and control, life insurance increasingly operates as the central anchor, with other structures used to complement rather than replace it.

Asia’s rapid wealth accumulation is colliding with a succession planning gap, characterised by limited use of wills, rising disputes and significant liquidity risk at generational transition. At the same time, regulatory scrutiny and cross-border mobility are increasing complexity.

In this environment, life insurance provides a portable, compliant and enduring framework that brings liquidity, governance and intergenerational continuity to the centre of holistic wealth planning.

Case Study Insights

Read the case study, Private Succession and Asset Integration Through Insurance-Based Solutions – a successful Chinese business founder with significant IPO wealth wants to protect business continuity for his successor while creating fair outcomes for a second child overseas, all while reducing fragmentation across banks and structures.

Visit the Case Study Insights section below, or click here.

Lana Jarvis

Senior Wealth Planner – UK

For UK-based and internationally mobile ultra-high-net-worth clients, planning is rarely static. It is typically triggered by change: a liquidity event, a relocation, succession planning or a shift in family dynamics. These moments expose a common underlying issue. Structures built incrementally can lack coherence when viewed as a whole.

Over time, clients often accumulate multiple solutions for different objectives. They may hold trusts, corporate entities, directly held assets and portfolios managed across multiple providers and jurisdictions. Each component may have been sensible in isolation. The challenge is that, collectively, these arrangements can create fragmentation, blind spots and friction at the precise moments when planning is tested.

The issues tend to surface in three situations: succession, mobility and liquidity. This is not necessarily a failure of advice. It is often a consequence of solving problems sequentially, without a single framework that ties the plan together.

1. Governance and decision-making risk

Different structures come with different decision-makers: trustees, directors, investment managers, family members and professional advisers. Where roles and responsibilities are not clearly aligned, decision-making slows. This can create inconsistency, delay and, in some cases, conflict. It also increases operational risk at the point a family needs fast, coordinated action.

2. Duplication, cost and lack of visibility

Clients frequently hold overlapping exposures across multiple vehicles. That reduces transparency and can make it difficult to answer basic questions quickly: What is owned, where is it held, who controls it and how is it accessed? Duplication can also increase cost, particularly where multiple structures require separate administration, reporting and governance.

3. UK tax outcomes are sensitive to residence and structure

UK planning does not operate in isolation. UK tax outcomes can be highly sensitive to residence and to the way assets are held. Where structures involve multiple jurisdictions, changes in residence (for the client or other relevant parties) can materially alter how arrangements are taxed or reported. A structure that works for a UK resident may become inefficient or problematic following relocation, particularly where control, attribution or reporting rules change.

4. Liquidity is often underestimated

Liquidity risk is consistently under-planned. In many cases, UK inheritance tax represents a cash liability that arises at death, while underlying assets may be illiquid or tied up across multiple vehicles. The result is a mismatch between the liability and accessible funds. Even where liquidity exists, delays in administration can be material. The distribution of a UK estate can remain heavily dependent on probate, and cross-border estates can add further complexity and delay.

Used appropriately, a life insurance policy can sit at the centre of a wider plan and address several structural weaknesses created by fragmented arrangements.

Consolidation under a single legal framework

A life insurance policy allows assets to be held centrally under one legal framework. This provides a clear point of coordination across a client’s wealth, rather than relying on multiple disconnected vehicles. Consolidation can improve visibility and reduce duplication, while still allowing the underlying investment strategy to be implemented within defined parameters.

Portability for internationally mobile families

Internationally mobile families often need structures that do not require repeated re-papering as residence changes. A life insurance policy can be designed to accommodate changes in residence without requiring a fundamental reorganisation of underlying assets each time a client moves. This can be a meaningful advantage where families have members in multiple jurisdictions, or where a move is likely over the planning horizon.

A more predictable route to accessing value

A life insurance policy can provide a mechanism through which value may be accessed in a controlled and more predictable way during life and on death. For UK resident clients, taxation is generally triggered by specific events (such as withdrawals, surrender or death), rather than annually on underlying portfolio movements. In addition, the structure can support smoother succession execution by aligning beneficiary planning and liquidity planning within the same framework.

None of this removes the need for complementary structures. Trusts, companies and directly held assets remain relevant depending on the client’s objectives, asset types and the need for governance or control. An insurance-based solution can help bring these objectives together within a coherent framework, reducing reliance on disconnected arrangements.

It is also important to recognise the increasing focus on confidentiality. Wills may become public on probate, and the value and distribution of assets can become visible. In this context, structures that support discretion, clearly defined roles and orderly wealth transfer can be particularly valuable for ultra-high-net-worth families.

For UK clients, fragmented planning creates predictable pressure points: governance friction, uneven tax outcomes and liquidity shortfalls at the wrong time. An insurance-based wealth solution can act as the central anchor, bringing greater coherence, portability and control to complex wealth structures, while complementary tools continue to play their role.

Aidan Golden

Head of Group Technical Services

Stephen Atkinson

Global Head of Sales and Marketing, Utmost

As private market assets move from the margins into the core of high-net-worth portfolios, the structures used to hold them and the governance that supports those structures are coming under increasing scrutiny.

In this interview, Aidan Golden talks to Stephen Atkinson, Global Head of Sales and Marketing at Utmost, about how the expectations of regulatory authorities are evolving, what this means for advisers and trustees, and why good outcomes increasingly depend on how assets are administered, valued and funded over time, not just on what is being invested in.

AG : Private markets are now widely seen as a core allocation for HNW investors. What has changed, and why are regulatory authorities paying closer attention?

SA : Private markets have grown up. Ten or fifteen years ago, they were largely the preserve of institutions and a small number of sophisticated family offices. Today, they are a central part of portfolio construction for many high-net-worth and ultra-high-net-worth investors.

From a regulatory perspective, that shift matters. As private assets move from the periphery into the mainstream, the focus broadens from individual investment decisions to the structures and systems supporting those investments. Regulatory authorities are asking whether long-term promises to policyholders are being supported by appropriate governance, valuation discipline and liquidity management.

This is not about discouraging investment in private markets. It is about recognising that these assets behave very differently from listed securities and ensuring the infrastructure holding them is genuinely fit for purpose.

AG : When regulators talk about risk in this context, what risks are they really concerned about?

SA : It is rarely about the investment idea itself. More often, the focus is on how assets are held, governed and managed over time.

Regulators are increasingly concerned with valuation discipline, liquidity management and counterparty strength. Private assets are not priced daily and do not offer predictable exit routes. As a result, the risk sits less in short-term market movements and more in how those assets are administered within a structure.

We are also seeing regulators push back on informal or overly bespoke interpretations of risk. Recent regulatory clarification in other areas of the insurance market reinforces a consistent message. When insurance structures are involved, the focus is firmly on the legal and economic reality of the structure and on the insurer standing behind it, rather than on looking through to underlying assets or assumptions.

That same mindset is now being applied more broadly as private assets become mainstream within wealth structures. Governance, operational capability and financial strength matter just as much as asset selection if long-term outcomes are to be protected.

AG : Liquidity is often misunderstood with private assets. Where do advisers most commonly misjudge it?

SA : The most common mistake is assuming that a product’s liquidity features are the same as the liquidity of the underlying assets.

Some structures appear to offer smoother access or periodic liquidity, but the assets beneath them remain fundamentally illiquid. That mismatch can create pressure if investor behaviour changes or market conditions deteriorate.

Insurance-based structures, by contrast, are inherently long-term. They are designed around extended investment horizons and structured liquidity management, which aligns more closely with the reality of private market investing. That alignment can significantly reduce the risk of forced asset sales during periods of stress.

For advisers, the key is understanding not just when clients can access capital, but how that access is funded and what assumptions sit behind it.

AG : Valuation is another area attracting the attention of regulators. What should advisers and trustees be aware of?

SA : Valuation in private markets is necessarily imperfect, but that does not mean it can be casual.

Advisers and trustees should understand how valuations are produced, how often they are refreshed and how they are challenged. Are independent valuations used? How are model assumptions reviewed? How are valuation lags reflected at policy level?

Within an insurance framework, valuation discipline is reinforced by regulatory capital requirements and governance processes. That does not remove uncertainty, but it does introduce structure, consistency and accountability, which is exactly what regulators are looking for.

AG : Operational capability comes up repeatedly. What differentiates insurers that can safely hold complex assets?

SA : Experience and scale matter a great deal. Holding private assets is not just about custody. It involves managing cashflows, capital calls, distributions, valuations and reporting over many years, often across multiple jurisdictions.

Insurers that have invested in specialist teams, robust operating models and strong external partner networks are far better placed to absorb that complexity without passing unnecessary risk on to clients or trustees.

From an oversight perspective, it is no longer enough to assess an insurer’s financial strength alone. What really matters is whether the insurer has the right operational depth and governance, supported by experienced investment and technical teams, to administer complex assets throughout the life of a policy.

AG : For trustees and advisers, what does “good oversight” look like in practice today?

SA : It does not mean becoming a private markets specialist. But it does mean asking better questions.

Trustees and advisers should expect clear answers on asset eligibility, valuation processes, liquidity management and governance arrangements. They should understand how capital calls are funded, how cash buffers are managed and how risks are monitored over time. Importantly, oversight is shifting from a product-centric exercise to a system-level one. It is about understanding the ecosystem supporting the investment, not just the investment itself.

AG : Are there any red flags advisers should watch for?

SA : Over-promising on liquidity is a major one, as is a lack of transparency around valuation methodology or operational processes.

Another red flag is when complex assets are introduced without a clear explanation of how they will be administered over time. If the operational story is unclear, that is usually a warning sign.