This briefing is designed for financial advisers only and should not be distributed to or relied upon by individual investors.

This briefing is designed for financial advisers only and should not be distributed to or relied upon by individual investors.

Aidan Golden

Head of Group Technical Services

Welcome to the second edition of Navigator, your trusted source for international industry insights and updates on insurance-based wealth solutions.

Since the launch of Navigator in October 2024, we have been encouraged by the positive feedback we have received. In an ever-evolving landscape, staying informed and adaptable is more crucial than ever. Your support motivates us to continue delivering valuable content in this and future editions.

The current tax and regulatory environments are in a state of constant flux, presenting both challenges and opportunities for our industry. This edition underscores the importance of having a robust technical team to keep abreast of these changes and to assist our partners and their clients in not only staying informed but also in understanding the implications of these developments.

One of the most significant changes in the tax environment is the revamp of the UK non-dom regime. With the upcoming 5 April 2025 deadline, we have included an in-depth analysis to help clients prepare and plan effectively. Additionally, the regulatory landscape is shifting, as evidenced by recent changes in France with the Green Law impacting the advisory model, and in Italy with potential new permissible asset regulations. These topics are covered in detail in this edition, though they continue to evolve.

We are also pleased to feature a contribution from Stephen Atkinson, our Global Head of Sales and Marketing, on the growing private market asset investment sector. His insights into the latest trends, risks, and opportunities are invaluable for advisers looking to navigate this complex area.

Furthermore, we welcome contributions from our new Luxembourg colleagues, whose expertise has significantly broadened the scope and depth of our technical team. Their insights are a testament to our commitment to providing comprehensive and informed guidance to our partners.

We hope you find this edition of Navigator both informative and engaging. As always, we are here to support you in delivering the best possible outcomes for your clients.

Aidan Golden

Glenn McIlroy

Technical Manager

Brendan Harper

Head of Asia and HNW Technical Services

Pension policy in the UK has undergone significant shifts recently, reflecting a change in government and differing priorities. The first Labour budget in 14 years expanded taxation on pensions, moving away from the Conservative approach of encouraging pension savings and longer workforce participation.

Let’s look at what has changed over the past two years and examine the impact on pension savers in the UK and beyond.

Nerea Llona

Tax and Legal Counsel, Spain and LatAm

The Spanish government has officially announced the termination of the Golden Visa – investor visa scheme. This significant change, published in the Spanish Official Gazette on 3 January 2025, will come into effect on 3 April 2025. This update provides crucial information on the upcoming changes.

Filippo Mancini

Senior Wealth Planner, Italy

Filippo Mancini examines the latest regulatory shift by IVASS, which proposes new investment limits for unit-linked insurance products. This development challenges the principle of home country control and raises important questions for EU insurers, particularly those based in Luxembourg and Ireland.

Nicolaas Vancrombrugge

Senior Wealth Planner, Belgium and Luxembourg

Nicolaas Vancrombrugge looks at the latest developments in the Luxembourg Branch 6 capitalisation contract and the ongoing regulatory debate with the Belgian Financial Regulator (FSMA). This article explores the implications for Belgian corporate entities and the positions of both the FSMA and the Luxembourg insurance sector.

Glenn McIlroy

Technical Manager

Brendan Harper

Head of Asia and HNW Technical Services

Pension policy in the UK has undergone significant shifts recently, reflecting a change in government and differing priorities. The first Labour budget in 14 years expanded taxation on pensions, moving away from the Conservative approach of encouraging pension savings and longer workforce participation.

In their last year of government, the Conservatives made significant legislative changes affecting pensions. Their aim was to encourage pension saving while retaining limits on tax-free pension benefits through measures including the removal of the Lifetime Allowance (LTA). The LTA, previously capped at £1,073,100, was seen as a disincentive for high earners to continue working. Its removal aimed to encourage longer workforce participation, addressing labour shortages in key sectors such as the NHS.

Despite the removal of the LTA, tax-free cash withdrawal limits remain, facilitated by three new allowances:

Before April 2024, a transfer to a QROPS was tested against the LTA as a benefit crystallisation event. With no prior crystallisation event, it was possible to transfer £1,073,100 to a QROPS tax-free, with any excess subject to a 25% LTA charge. The removal of the LTA could have led to pensions of unlimited value transferring tax-free to a QROPS. To prevent this, all transfers to overseas pensions are now tested against the OTA, with any excess subject to a 25% overseas transfer charge.

Existing LTA protections can be applied to the LSA and LSDBA calculations.

The taxation of death benefits post-age 75 remains the same, taxed at the beneficiary's marginal rate. For deaths occurring before age 75, changes include:

For individuals with crystallised benefits pre-April 2024, transitional rules ensure they are not worse off regarding tax-free cash.

Removing the lifetime allowance encouraged high earners to continue working and saving. However, introducing IHT on unused pensions changes this dynamic, discouraging wealth retention in pensions for succession planning. Instead, the government aims to ensure tax reliefs support retirement income savings.

High-value UK pension holders and expats must reassess financial plans. The removal of IHT incentives may lead to earlier pension withdrawals. UK expats in low-tax countries might fully access pensions to avoid UK tax liabilities and use alternative, tax-efficient products, such as offshore bonds for future withdrawals. This shift opens new planning opportunities aligned with the evolving pension landscape.

Nerea Llona

Tax and Legal Counsel, Spain and LatAm

The Spanish government has officially announced the termination of the Golden Visa – investor visa scheme. This significant change, published in the Spanish Official Gazette on 3 January 2025, will come into effect on 3 April 2025. This update provides crucial information on the upcoming changes and their implications for non-EU/EEA clients considering this route to residency in Spain.

The Spanish Golden Visa scheme, which has been a popular pathway for non-EU/EEA investors to obtain residency in Spain, will be eliminated from 3 April 2025. Applications submitted before this date will be processed under the existing rules, and any visas or residence permits granted before 3 April 2025, will remain valid until their expiration. Renewal applications for existing Golden Visas will continue to be assessed based on the regulations in place at the time of the initial grant.

This change means that there are only three months left to submit new applications under the current scheme. Non-EU/EEA clients who are considering this option should urgently consult with an immigration lawyer to understand their options and ensure their applications are submitted in time.

The removal of the Spanish Golden Visa scheme marks a significant shift in Spain's immigration policy. Advisers should proactively reach out to their clients who may be affected by this change to provide guidance and support. With the deadline fast approaching, timely action is essential to navigate this transition smoothly.

Filippo Mancini

Senior Wealth Planner, Italy

On 28 March 2024, IVASS (Istituto per la Vigilanza sulle Assicurazioni) published the results of its first public consultation on the proposed investment limits for unit-linked insurance products, together with a new draft regulation under consultation. This marks a significant regulatory shift, as for the first time the Italian regulatory framework on investment limits may apply to EU-based insurers operating cross-border.

Such a development challenges the established principle of home country control and raises important questions for EU insurers, especially Luxembourg and Ireland-based companies.

EU insurers have played a complementary role in the Italian market for decades, offering compliant wealth management solutions like Internal Dedicated Funds (IDFs). These bespoke structures, tailored to meet the needs of affluent clients with often multifaceted circumstances, have traditionally operated under local regulatory supervision, in line with EU principles.

However, the proposed IVASS regulation aims to harmonise investment limits for unit-linked policies across all players, citing enhanced consumer protection and a level playing field as its primary objectives. This broader scope, though, introduces new challenges, particularly in its application to investment structures like IDFs, which differ significantly from collective investment schemes typical of the Italian market.

The feedback provided by IVASS in response to industry comments upon first consultation reflects a nuanced, yet ambiguous position. On one hand, IVASS seems to imply that IDFs may fall outside the regulation’s scope. On the other hand, it reiterates that premiums collected in unit-linked policies are subject to collective management by the insurer. This dual interpretation has left market participants unsure about the actual reach of the proposed rules.

The value proposition of EU-based insurers, known for their flexibility and adaptability to international regulatory frameworks, now faces a critical juncture. The new IVASS proposals, while focused on enhancing retail consumer protection, introduce elements that could impact the operations of core products such as IDFs, with the risk of limiting the range of international products offered to Italian customers.

This regulatory evolution requires careful assessment by EU-based operators, who have consistently excelled in delivering innovative and tailored solutions. Engaging in constructive dialogue with IVASS may help clarify ambiguities while ensuring that the efficiency and relevance of the international model remain intact. It is essential for the sector to continue demonstrating its ability to meet the needs of a multifaceted international clientele, reinforcing its commitment to transparency and stability.

In an evolving regulatory context that moves toward greater uniformity, EU insurers have an opportunity to strengthen their collaboration with Italian authorities and other European stakeholders. A proactive and unified approach could help address potential uncertainties, ensuring that the unique features of more specialised products are understood and appreciated.

At the same time, it is crucial to ensure that the regulatory framework does not introduce rigidities that could constrain the insurers’ operations. Greater clarity from IVASS regarding the practical application of the new rules could provide the foundation for a balanced transition, enabling operators to continue working efficiently while preserving client trust and the competitiveness of the cross-border market.

The proposed IVASS regulation highlights the growing divergence between national regulatory priorities and the realities of cross-border markets. For several years, EU insurers have demonstrated resilience and adaptability in integrating into diverse regulatory environments. However, this latest development underscores the importance of proactive engagement and long-term strategic planning to maintain their competitive edge in the Italian market.

Nicolaas Vancrombrugge

Senior Wealth Planner, Belgium and Luxembourg

The Luxembourg Branch 6 capitalisation contract is a crucial financial product for Belgian corporate entities. Managing an investment portfolio directly in a securities account by a Belgian entity involves significant administrative and tax burdens. These complexities can be mitigated if a Belgian entity transfers its investment portfolio into a Branch 6 unit-linked capitalisation contract. In this arrangement, the insurance company manages the portfolio according to the subscriber's preferences or, in most cases, delegates its management to a discretionary asset manager, all in compliance with Belgian regulations.

The tax regime applicable to the Branch 6 capitalisation contract for Belgian entities has been a long-debated issue, with various contradictory rulings from the Belgian tax administration. This debate was resolved when the Belgian legislator clarified the tax regime through a law enacted at the end of 2023. Since 2024, Branch 6 capitalisation contracts subscribed by Belgian entities enjoy tax certainty.

Lombard International Assurance, now part of Utmost Group, introduced its Branch 6 capitalisation contract to the Belgian market in late 2021 from its Luxembourg head office, followed by its Belgian branch in 2022. This product is specifically designed for legal entities and cannot be subscribed to by individuals. The product's appeal to Belgian legal entities lies in its ability to simplify administrative processes while providing tax certainty, leading to growing interest and potential in this solution.

In 2019, the Belgian Financial Regulator (FSMA) first notified some Luxembourg insurance companies offering the Branch 6 capitalisation contract that it did not agree with the product's distribution in Belgium. FSMA based its stance on a strict and arguably debatable interpretation of the EU Solvency II regulation, concluding that capitalisation products must have a fixed return to fall under the EU freedom of services provisions for insurance products as defined by the Solvency II Directive.

However, Belgian law, which transposed the Solvency II Directive into national legislation in 2016, explicitly includes a broader definition of capitalisation contracts. This definition encompasses not only fixed-return contracts, but also unit-linked contracts tied to investment funds.

In March 2024, FSMA reiterated its position by sending a new round of letters to Luxembourg insurance companies, advising them to seek clarification from the European Insurance and Occupational Pensions Authority (EIOPA) on the interpretation of the Solvency II Directive. In November 2024, FSMA further communicated its stance to a number of Belgian insurance intermediaries, causing further uncertainty within the intermediary network.

In response to the growing uncertainty among Belgian intermediaries, the Luxembourg Association of Insurance and Reinsurance Companies (ACA) engaged in extensive discussions on the matter in December 2024. On 8 January 2025, ACA issued an official statement asserting that FSMA's position is unjustified as it contradicts applicable legislation and violates EU principles of freedom to provide services and free movement of capital.

ACA concluded its statement by affirming that it will take the necessary steps to defend the right of Luxembourg life insurance companies to distribute Branch 6 capitalisation contracts in Belgium and ensure that Belgian clients can access these products.

In the meantime, it appears that FSMA has itself raised the issue with EIOPA. Consequently, the interpretation of the Solvency II Directive concerning capitalisation contracts is expected to be addressed at the European level, potentially involving both EIOPA and the European Commission.

The ongoing debate between the FSMA and Luxembourg insurance companies over the Branch 6 capitalisation contract underscores the complexities of cross-border financial regulations within the EU. As the situation evolves, it is crucial for Belgian corporate entities and their advisers to stay informed and prepared for potential changes. The outcome of this debate will impact the distribution and accessibility of these financial products in Belgium.

Simon Martin

Head of UK Technical Services

Simon Martin, Head of UK Technical Services, provides an overview of the key personal taxation measures from the UK Autumn Budget and their implications for investors and estate planning.

Brendan Harper

Head of Asia and HNW Technical Services

Amid predictions of a mass exodus of foreign HNW individuals from the UK following the UK Budget, long-term UK expatriates have a reason to celebrate.

Brendan Harper, Head of Asia and HNW Technical Services, explains how the break in the link between UK domicile and Inheritance Tax significantly benefits expatriates, allowing them to plan with certainty and avoid the complexities of the old tax regime.

Jari Vill

Tax and Legal Counsel – Scandinavia

Unit-linked life insurance offers significant benefits and flexibility for clients in Finland, providing long-term savings and investment solutions. With advantages such as gross roll-up, VAT exemption on asset management fees, and simplified inheritance planning, these policies are designed to meet the needs of a mobile and international population.

Jari Vill, Tax and Legal Counsel – Scandinavia, explains the tax implications and compliance requirements for clients when moving to or from Finland and how advisers can help maximise the benefits of their life insurance policies through proper planning and adherence to local regulations.

Peter Tung

Tax and Legal Counsel – Asia

Sustainable wealth management is crucial for high-net-worth (HNW) families in Asia, given their unique and complex needs. In this article, Peter Tung looks at the strategies for securing long-term financial health, optimising wealth transfer, and maintaining privacy amid evolving regulatory environments.

Ester Carbonell van Reck

Wealth Planner – Spain, Portugal and LatAm

The Spanish Supreme Court has recently issued two significant decisions regarding the legal nature and tax implications of unit-linked life insurance contracts. These rulings clarify that unit-linked contracts are indeed life insurance contracts and, before 2021, were not subject to Spanish Wealth Tax if they had no right of surrender.

In this article, Ester Carbonell van Reck examines the details and implications of these decisions.

Nerea Llona

Tax and Legal Counsel, Spain and LatAm

Nerea Llona examines Spain's 2025 tax rate increase for savings income and capital gains. Effective 1 January 2025, the maximum Personal Income Tax rate for savings income and capital gains exceeding €300,000 will increase from 28% to 30%. In this update, Nerea provides the relevant information on these upcoming changes.

Jari Vill

Tax and Legal Counsel – Scandinavia

Discover the key updates to Sweden's yield tax rate for 2025 and what it means for the life insurance policies of Swedish clients.

Simon Martin

Head of UK Technical Services

As widely speculated before the Budget, there was a significant increase in Capital Gains Tax (CGT) rates. The basic and higher rates have moved from 10% and 20% to 18% and 24%, respectively. Furthermore, the dividend allowance, initially introduced in 2016/17 at £5,000, has been reduced by previous Budgets and now stands at only £500. These measures, along with continual squeezes in the CGT annual exempt amount, will make unwrapped investments less attractive to many savers.

From 6 April 2025, a person’s estate will become potentially liable to UK Inheritance Tax (IHT) on death if they’ve been a UK tax resident for 10 out of the last 20 tax years. The test for tax residence will use the existing statutory residence test, which should remove the uncertainty and complexity that previously surrounded the domicile-based regime. Additionally, the Budget confirmed the removal of the remittance basis of taxation from 6 April 2025 and various trust protections.

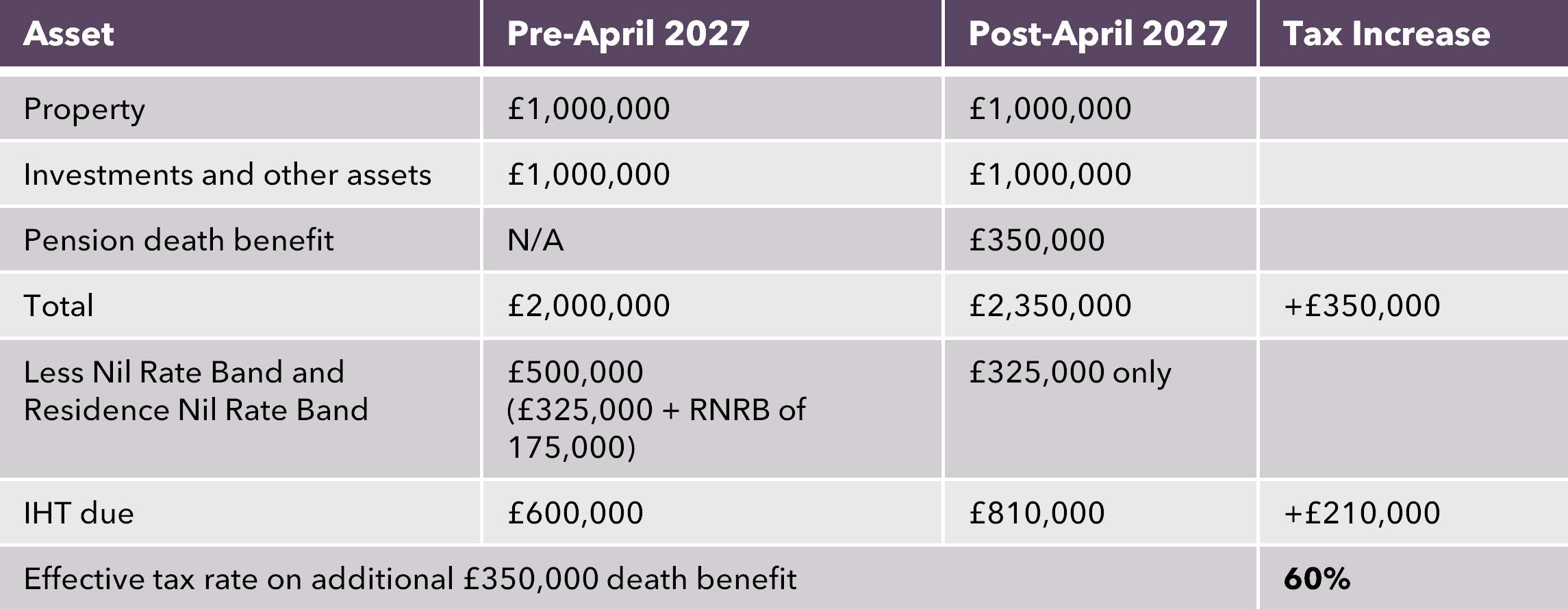

More surprisingly, it was announced that unused pension funds and death benefits will be subject to IHT from 6 April 2027, with a consultation released around its implementation.

For clients who have always been UK residents, most of these changes will make little difference. However, there’s an additional tax trap for some larger estates due to the RNRB tapering provisions, where the amount of RNRB available is reduced by £1 for every £2 that the estate exceeds £2 million. The addition of pension funds from April 2027 could lead to an effective tax rate of 60%, as illustrated in the table below:

With careful financial planning, the impact of the changes can be mitigated for clients. Insurance policy wrappers can allow clients to defer tax liabilities, which will now be of interest to a wider population given the CGT changes. Insurance policies can also be used alongside trust solutions to help reduce exposure to UK IHT.

A full briefing, compiling the announcements made in the October Budget along with many changes announced over the past year, is available below.

Brendan Harper

Head of Asia and HNW Technical Services

Amid the “doom and gloom” predictions of a mass exodus of foreign HNW individuals from the UK following the UK Budget, one client segment is celebrating – long-term UK expatriates. The break in the link between UK domicile and Inheritance Tax (IHT) significantly benefits them.

Under current rules, an individual with a UK domicile of origin retains it until they settle elsewhere and adopt a new “domicile of choice”.

Until then, their worldwide estate remains potentially subject to UK IHT. This creates a major challenge for long-term expatriates who may not intend to stay permanently in their current country, as they cannot lose their UK domicile of origin, even if they don’t plan to return to the UK.

Even when they take steps to adopt a new domicile of choice, there's always uncertainty about whether they've done enough to shed their domicile of origin. If they ultimately leave their adopted domicile, their domicile of origin revives itself.

This outdated basis for taxing an individual’s estate complicates financial planning, as potential UK IHT must always be considered. For example, it can prevent clients from creating trusts for family wealth protection, as transfers above £325,000 can result in a 20% IHT entry charge.

From 6 April 2025, this will change. UK IHT on non-UK assets will only be levied if the transferor has been resident in the UK for at least 10 out of the previous 20 years. This “tax tail” can be as little as three years if, before relocating overseas, the individual had been resident in the UK for more than 10 but less than 19 years.

Long-term expatriates no longer have the “sword of Damocles” of a domicile of origin hanging over them, worrying whether they've done enough to adopt a domicile of choice elsewhere to escape UK IHT on their worldwide estate.

This means expatriates can plan with certainty, including creating trusts for legitimate reasons unrelated to tax, such as protecting wealth and loved ones. They can do so without the fear of IHT entry charges. They can also plan based on the country they intend to settle in, without needing to factor in UK IHT.

Furthermore, if they return to the UK after 10 consecutive years’ non-residence, their overseas assets will remain outside the UK IHT net for a further 10 years, giving them ample time to put a long-term planning strategy in place.

In this scenario, a bond from Utmost Wealth Solutions could be a perfect holding vehicle that will remain outside the IHT net, with the ability to transfer it to a suitable trust as the policyholder approaches the 10-year point.

Jari Vill

Tax and Legal Counsel – Scandinavia

Unit-linked life insurance provides a long-term savings and investment solution in Finland, offering clients and their beneficiaries unique benefits and flexibility.

Clients benefit from gross roll-up, allowing them to invest in a diverse range of assets and make changes to their investments freely and tax-free. Accumulated gains are only taxed when funds are withdrawn from the policy and are subject to capital gains tax in Finland. Furthermore, losses on a full surrender may be deducted from their capital gains tax liability in the tax year or carried forward for up to 10 years.

Policies from an Irish insurer also benefit from VAT exemption on asset management fees. Furthermore, life insurance simplifies inheritance planning by allowing policyholders to directly transfer assets to their chosen beneficiaries. Unlike a will, where assets become part of the estate, life insurance ensures that beneficiaries receive the assets directly upon death, enabling quick access to death benefits.

Given the growing mobile and international population, families often relocate across several jurisdictions during their lifetimes. Consequently, long-term wealth solutions must be portable to meet client expectations.

Unit-linked life insurance products, such as those offered by Utmost Wealth Solutions, are designed to facilitate this portability. When a policyholder changes their country of residence, these products allow tax benefits to be maintained without having to surrender or restructure the policy.

Finland has signed tax treaties with around 70 countries, primarily based on the OECD’s model tax treaty.

When a citizen of Finland moves abroad, the "three-year rule" in the Income Tax Act usually applies. They are typically regarded as a resident taxpayer in Finland for the year they move away and the following three years. They may be considered a non-resident taxpayer before the end of the third year if they claim non-resident status and demonstrate no substantial ties with Finland during the tax year. A permanent move is key to breaking substantial ties.

It is essential to assess clients’ personal circumstances thoroughly before moving jurisdictions to avoid unfavourable tax and regulatory consequences. Clients should ensure their policy features, such as biometric risk, investment model, asset permissibility, and beneficiary nomination, are compliant in the destination country.

In 2022, the Finnish government proposed an exit tax that would have subjected individuals with significant non-real estate assets, including life insurance policies, to capital gains tax on the increased value of their assets when leaving Finland. This proposal was removed from the legislative plan, with no indication it will be reintroduced in the near future.

Previously, Finland and Portugal had a double tax treaty in force affecting pension taxation. The Portuguese Non-Habitual Tax Resident Regime, which was in force until 31 December 2023, featured a reduced flat tax rate of 10% for non-Portuguese sourced pensions. Following its expiry on 31 December 2018, persons living in Portugal who receive a pension from Finland pay tax in Finland and may need to apply for a tax credit in Portugal for the Finnish tax.

When clients move to Finland and wish to keep their foreign life insurance compliant, they should ensure policy features like biometric risk and beneficiary nomination align with Finnish requirements. Key points to consider include:

Taxable Gain: Under the Finnish Income Tax Act 1535/1992, only the gain from a life insurance policy is taxable if:

Special Tax Treatment of Certain Insurances: Section 35b of the Income Tax Act states that the gross roll-up benefit of life insurance policies can be lost if the policyholder or an appointed person has rights over the underlying assets. These include:

The condition is deemed to be fulfilled if the policyholder or an appointed person has exercised any of these rights during the tax year, if the agreement provides for the exercise of such rights, or if the actual possibility of exercising such rights exists.

Therefore, to avoid misinterpretation, policy documents and features must ensure:

Unit-linked life insurance offers significant benefits and flexibility for clients in Finland, providing long-term savings and investment solutions.

Contact your Utmost Wealth Solutions sales representative to discuss how our tailored life insurance solutions can help you maximise these benefits and navigate the complexities of tax and regulatory requirements seamlessly.

Peter Tung

Tax and Legal Counsel – Asia

Sustainable wealth management is crucial for high-net-worth (HNW) families, given their unique and complex needs. Many Asian HNW families are entrepreneurially driven, with wealth originating from active business ventures that transition into private assets. The diversity in family sizes and structures, influenced by policies like China’s former one-child policy, presents unique challenges compared to Western counterparts, requiring tailored strategies to address these specific dynamics.

Sustainable wealth management aims to secure long-term financial health while meeting both economic and personal needs. This requires flexibility and robust governance to manage risks, including legal and tax obligations, as regulatory environments evolve. It involves optimising wealth transfer across generations, ensuring structures align with your client's evolving objectives. Clients and their advisers must stay agile and informed to navigate these complexities effectively.

Many Asian HNW families prefer simpler offshore structures like private investment holding companies (PICs) for their ease of setup, administrative efficiency, and privacy. However, these structures face increasing scrutiny due to global transparency initiatives. Trusts, though less common in Asia, can be effective for asset protection and controlled wealth distribution if structured properly. Anticipating regulatory changes and adapting strategies accordingly is crucial.

Privacy and efficient wealth transfer are key drivers for Asian HNW clients. Privacy is highly valued, especially amid increasing regulatory transparency requirements. Efficient wealth transfer is crucial for families with complex, cross-border investments. Holding assets under an appropriate structure that fits your client's family needs can simplify inheritance and bypass probate processes. Suitable insurance solutions like Private Placement Life Insurance (PPLI) and Variable Universal Life (VUL) policies can help mitigate tax liabilities and support efficient wealth transition, allowing clients to maintain their privacy and streamline wealth transfer.

Family offices play a valuable role in wealth management, particularly for investment delegation. They can oversee investment decisions within a PPLI policy, ensuring asset allocations align with your client's risk tolerance and financial goals. A family office, with assistance from wealth professionals, can significantly enhance the management and preservation of your client's family wealth.

To learn more about how these strategies can be tailored to your client's unique needs, contact your Utmost Wealth Solutions sales representative to discuss these insights further and help you to navigate the complexities of sustainable wealth management.

Ester Carbonell van Reck

Wealth Planner – Spain, Portugal and LatAm

On 14 October 2024, the Spanish Supreme Court issued two decisions overturning Galicia’s High Court judgments. These rulings confirmed that unit-linked contracts are legally considered life insurance contracts. Additionally, the Court concluded that, before 2021, unit-linked life insurance contracts without a right of surrender were exempt from Spanish Wealth Tax.

These two decisions, with identical content, relate to taxpayers who had taken out ‘mixed-term’ unit-linked life insurance policies, which include both survival and death cover. In these policies, the policyholder is designated as the irrevocable beneficiary in the event of survival, and his/her heirs are the irrevocable beneficiaries in the event of death.

Firstly, the Supreme Court defined unit-linked life insurance as genuine insurance operations, rejecting the lower court's argument that these contracts should be reclassified as ‘mixed products’ with a predominant investment purpose. The Court emphasised that, despite their high savings and low-risk components, Unit-linked contracts are life insurance contracts as per EU Directives and CJEU case law.

Secondly, the Court's decisions addressed the long-standing debate on whether unit-linked life insurance policies without a right of surrender should be taxed under Wealth Tax. According to Article 17 of Law 19/1991, life insurance policies were to be valued at their surrender value as of 31 December. The absence of a surrender value in certain unit-linked contracts had led to confusion and divergent rulings by administrative bodies and higher courts.

Despite administrative doctrine favouring non-taxation in the absence of a surrender value, some High Courts, like Galicia’s, had subjected these policies to Wealth Tax. They argued that the policy's asset value remained within the policyholder’s estate, affecting their wealth and economic capacity to pay.

The Supreme Court has ruled that the true legal nature of unit-linked life insurance contracts must be linked to the valuation rule of Article 17.1 of the Wealth Tax Law. In the absence of a surrender value, no Wealth Tax is applicable for tax years up to 2020.

However, an amendment to Article 17 on 11 July 2021 now requires unit-linked policies without a right of surrender to be valued at their mathematical provision value as of 31 December each year.

These Supreme Court decisions provide much-needed clarity on the legal nature and tax treatment of unit-linked life insurance contracts in Spain. They establish binding jurisprudence for future interpretation and application of the law, customs, and general principles of law. Advisers should take note of these rulings to ensure compliance and optimise their clients’ tax planning strategies.

Nerea Llona

Tax and Legal Counsel, Spain and LatAm

On 21 December 2024, Law 7/2024 of 20 December (“Law 7/2024”) was published in the Spanish Official State Gazette. In addition to regulating the Complementary Tax that ensures a global minimum level of taxation for multinational and large national groups (transposing Council Directive 2022/2523 of 15 December 2022, also known as “Pillar 2”), it introduces significant tax developments for Spanish taxpayers.

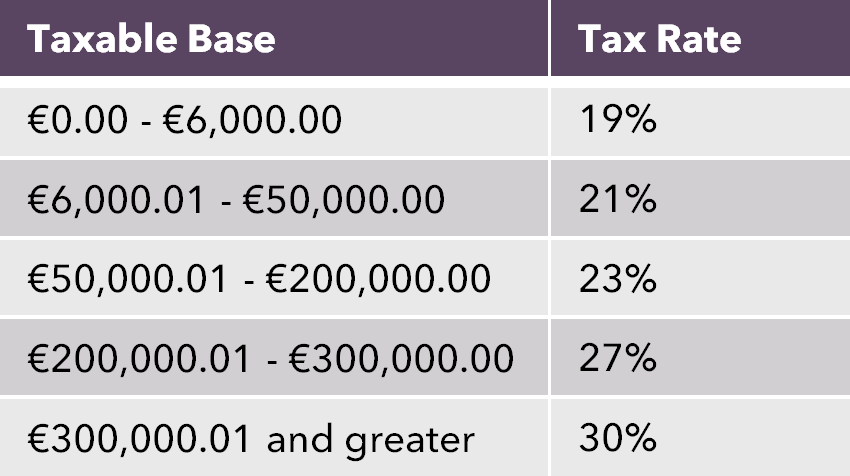

For individual taxpayers, Law 7/2024 increases the tax rate for taxable income exceeding €300,000 included in the Personal Income Tax savings base (e.g., interest income, dividends, income from life insurance, capital gains). Effective 1 January 2025, the highest tax band (income/gains above €300,000) will see an increase of two percentage points, from 28% to 30%.

The applicable tax rates for savings income and capital gains for Spanish tax residents from 1 January 2025 onwards are as follows:

This increase applies to all Spanish tax resident individuals, including those benefiting from the special tax regime, also known as the ‘Beckham Law’. The rest of the Personal Income Tax rates for general income and savings income/capital gains remain unchanged for Spanish resident taxpayers during the 2025 tax year.

Given this change, it is more important than ever for Spanish resident taxpayers to invest in assets or products that offer Personal Income Tax deferral benefits, such as unit-linked life assurance products.

In summary, the increase in the maximum Personal Income Tax rate for savings income and capital gains highlights the need for strategic tax planning. Spanish resident taxpayers should consider leveraging tax-smart investment products to mitigate the impact of this change.

Jari Vill

Tax and Legal Counsel – Scandinavia

If your clients have a Swedish life insurance policy to which they have paid premiums after 31 December 1996, they are obliged to pay Swedish yield tax.

This annual tax means your clients’ money is taxed annually and then ready for tax-free withdrawals. Income and capital gains arising from the funds and securities underlying the policy are not taxable, and there is no obligation to declare the transactions.

The taxation is based on an assumed annual yield corresponding to the government loan interest rate, plus 1% (from 2018, the total must not be below 1.2%). For the end of November 2024, the Swedish National Debt Agency set the government loan interest rate at 1.96%. This means the annual Swedish yield tax for the fiscal year 2025 will be 0.888% ([1.96 + 1.00] x 30%).

Starting 1 January 2025, policyholders will benefit from a tax-free allowance of SEK150,000, meaning the first SEK150,000 of their policy value (together with other policies and ISK accounts they hold) will be exempt from yield tax. This exemption will increase to SEK300,000 by 2026, further enhancing the attractiveness of life insurance as a tax-efficient wealth planning tool in Sweden.

To learn more about how these changes affect your clients and to tailor these insights to their unique needs, contact your Utmost Wealth Solutions sales representative for expert guidance.

Stephen Atkinson

Global Head of Sales and Marketing

Navigating global wealth trends can be challenging in the fast-paced financial services market. However, one promising area for financial advisers is the growing private market asset investment sector. This market is global, cross-border and expanding rapidly, though it comes with its own unique set of complexities and considerations.

In this article, Stephen Atkinson, Global Head of Sales and Marketing at Utmost Wealth Solutions, examines the latest trends, the risks and opportunities, and suggests how international bonds, paired with private asset investments, could serve as complementary planning tools.

Brendan Harper

Head of Asia and HNW Technical Services

Over 135,000 millionaires are predicted to migrate from their country of residence in 2025, with China and the United Kingdom1 seeing the largest outflows. These “net outflow” figures are counterbalanced by countries experiencing “net inflows”.

So, which countries are set to benefit from these inflows, what are the main attractions and considerations, and how can we help support you and your clients?

Stephen Atkinson

Global Head of Sales and Marketing – Utmost Wealth Solutions

In July 2024, research from Carne Group highlighted continued robust growth in private markets, projecting that the total value of global private market assets will reach $21.08 trillion by 2030. This represents a significant $8 trillion (or 62%) increase from today's figure, which is estimated at $13.01 trillion. Looking at the numbers again, this growth is particularly impressive considering that in 2005, global private market assets under management were around $1.6 trillion.

The surge in private market assets is driven by a growing investor appetite for alternative investments, which offer diversification and the potential for higher returns compared to traditionally public markets. In addition, private clients, especially wealthy individuals, are increasingly targeted by private equity funds, which up to now have only catered to institutional investors. These clients are drawn to private equity, real estate and other private market assets for their ability to generate substantial long-term gains.

Private markets play a significant role in the global economy, offering a myriad of opportunities for informed investors. Despite their substantial impact, they often remain less understood than their public market counterparts and do come with their own set of risks.

For example, liquidity risk. Unlike public markets where assets can be quickly bought or sold, private market investments often involve longer investment periods and can be harder to sell quickly. However, these investments often have risks that don’t move in the same direction as regular stocks or bonds. Considered carefully, private market investments could help to mitigate overall investment risk.

Understanding both the rewards and risks is crucial for making informed decisions in private market investments. Financial advisers play a pivotal role in guiding clients through this complex landscape. With wealthy clients increasingly targeted directly by eager equity companies, how can financial advisers ensure they retain their clients and become part of this lucrative and growing market?

By staying informed about the latest trends and leveraging their expertise, financial advisers can effectively position private market investments as a viable option for their clients. This involves not only understanding the market dynamics but also being able to communicate the potential benefits and risks clearly. Additionally, advisers can explore innovative strategies, such as pairing international bonds with private asset investments, to offer a balanced and diversified portfolio.

For financial advisers managing the portfolios of wealthy clients, selecting the optimal structure to hold private market assets is crucial. An international bond stands out as a potentially efficient vehicle for several compelling reasons:

To demonstrate how this solution works, read the case study ‘Maximising Returns for a Global Investor’ by Brendan Harper in the Case Study Insights section of this publication.

In conclusion, the private market asset investment sector presents a compelling opportunity for financial advisers and their clients. By understanding the intricate balance of risks and rewards, advisers can navigate this complex landscape effectively. The role of the financial adviser is crucial in helping clients make informed decisions, especially as wealthy individuals become prime targets for equity companies.

To capitalise on this growing market, advisers should stay abreast of the latest trends and consider innovative strategies, such as integrating international bonds with private asset investments. This approach can help create a diversified and resilient portfolio, positioning clients to benefit from the dynamic opportunities within the private market asset sector.

Brendan Harper

Head of Asia and HNW Technical Services

Over 135,000 millionaires are predicted to migrate from their country of residence in 2025, with China and the United Kingdom1 seeing the largest outflows. These “net outflow” figures are counterbalanced by countries experiencing “net inflows.”

You may be interested to know that Utmost Group has a presence in, or a portable value proposition for, at least seven out of the top 10 “net inflow” countries attracting globally mobile wealthy families. We also have coverage in six out of the top eight countries often cited as “safe havens,” an increasingly important consideration in wealthy families’ relocation plans.

So, which countries are set to benefit from these inflows, and what are the main attractions and considerations? Here are a few:

Attractions: Taking top spot with most predicted net inflows, the UAE rates highly on personal safety, ease of entry, and no personal taxes.

Considerations: Despite the UAE’s tax-free status, residents can become “accidental taxpayers” by failing to plan with their global investment portfolios. A big trap for the unwary is the lack of a double tax treaty with the US, potentially exposing UAE residents to US withholding taxes and Estate Tax on their US assets. Furthermore, the recently introduced corporation tax can apply to family investment companies, even if structured offshore. With planning, these problems are solvable.

Attractions: Climate, lifestyle, no Inheritance Tax.

Considerations: Recent dilution of the non-habitual residence regime means that fewer individuals will qualify to use this attractive tax regime, thus exposing their wealth to higher rates of tax. Although there is no inheritance tax, Portugal does have a 10% Stamp Duty which can bite on the transfer of certain assets on death. With careful planning, tax on investments can be driven as low as 11.2%, and assets can be passed on free of capital gains tax and stamp duty.

Attractions: Climate, lifestyle, and four special “expatriate” tax regimes, including an attractive regime for HNW individuals allowing them to pay a flat €200,000 in tax for 15 years.

Considerations: Expatriate regimes are designed to incentivise people to stay for the longer term. If a client chooses to do so, it’s important to consider structures that will last beyond the special tax “time bar”. Doing so can reduce income tax and inheritance tax exposure on wealth for the longer term.

Attractions: Personal safety; no personal taxes.

Considerations: Like UAE, individuals can become “accidental” taxpayers due to the lack of a double tax treaty network, and, in relation to succession planning, failure to consider the tax exposure in the countries where beneficiaries reside. Furthermore, there is inheritance tax in Monaco, which can apply even to foreign assets if these are not structured properly. With planning, these issues can be addressed.

Attractions: Climate, lifestyle, no Inheritance Tax.

Considerations: Whilst Australia has no inheritance tax, it does rank among the top jurisdictions for income taxes, with marginal rates of up to 47%. It also has wide-ranging anti-avoidance provisions that punitively tax offshore trust and company structures. With planning, however, it is possible to shelter investments in a way that reduces tax on investments to zero.

To learn more about how our tailored solutions can support your clients in these key destinations, contact your Utmost Wealth Solutions sales representative today.

Brendan Harper

Head of Asia and HNW Technical Services

In our Technical Spotlight section, Stephen Atkinson examined the growing private market asset investment sector and how international bonds, paired with private asset investments, could serve as complementary planning tools.

Selecting the optimal structure to hold private market assets is crucial for wealthy clients. This case study demonstrates how an international bond stands out as a potentially efficient solution.

A client, resident in Sweden, holds a large portfolio of listed securities and private market investments. These include private equity funds registered in the Cayman Islands with upcoming capital calls, hedge funds, and US property investment funds.

Each year, the client must report the income and gains accrued in these funds and pay tax at a flat rate of 30%. The Swedish Tax Authority frequently requests detailed information, often leading to discrepancies between the client’s tax return and the information the Authority receives via CRS, resulting in increased compliance costs.

Additionally, the client has been considering estate planning, aware of the complexities involved in distributing a multijurisdictional asset base, which could expose them to higher probate costs and possibly Estate Tax in the US.

To address these challenges, a private insurance policy from Utmost Wealth Solutions was implemented, designed to comply with Swedish tax and regulatory requirements. The client’s portfolio was consolidated into this policy, with private equity capital calls covered by a liquidity portfolio within the same policy.

This approach balanced the overall risk and changed the tax basis, allowing the client to pay an annual yield tax of 0.888% of the policy value each year. The Swedish Tax Authority can easily reconcile the policy value and transactions with the CRS report made by the insurance company.

Additionally, the client nominated beneficiaries to receive the policy death benefits, bypassing the need for probate in multiple jurisdictions.

The client benefited from enhanced tax efficiency, reduced administrative costs, and simplified estate planning.

Jari Vill

Tax and Legal Counsel – Scandinavia

Sofia, 43, and Peter, 58, have run a successful IT company in Sweden for 15 years. They recently sold the company and are now looking to manage the proceeds efficiently to minimise taxes when withdrawing funds. They have heard of the possibility of placing the proceeds into a holding company.

This case study explores the solution of placing the proceeds into a tailored offshore bond via a holding company and the benefits it offers.

Sofia and Peter's IT company was acquired by a major US firm for SEK 128,000,000. Prior to the acquisition, they transferred ownership to a newly established holding company, Holding AB, which they own equally.

Sofia will continue as Head of Sweden for the original company for at least three years and may start a new IT venture afterward. Peter will work as a consultant for three years before moving abroad with his wife to Italy, where he plans to reduce his workload and work independently.

Their requirements are:

After discussing with their financial adviser, they opted for a unit-linked life insurance solution for Holding AB using a Swedish Executive Portfolio (SEP) with Utmost Wealth Solutions.

In accordance with Swedish holding company rules, and to ensure easy and smooth accounting of transactions with a yield tax instead of corporate tax, the capital they received will be invested into the SEP and managed in the holding company on a discretionary basis.

Investing the proceeds into a SEP via a holding company offers several advantages:

Sofia has resigned to work independently in Sweden, and has transferred her ownership to a new holding company Holding II AB.

Peter and his wife have been living in the Italian Alps for two years.

Peter and Sofia have decided to liquidate Holding AB and assign segments to split the ownership as a dividend instead of cash. For that reason, they requested a bond split and a bond transfer of the existing policy.

After the bond split, half of the policy, with segments 1-50 and 50% of the assets, is transferred to Sofia´s new company Holding II AB.

The remainder of the policy, with segments 51-100 and 50% of the assets, is transferred to Peter in his own name. His wife and children become beneficiaries, and the policy is adapted to Italian rules. If they return to Sweden, the policy can continue under Swedish rules without needing a new policy.

For more details about this case study and our Swedish Executive Portfolio, please contact your Utmost Wealth Solutions sales representative.

Market

Event

Date

UK

Utmost Wealth Solutions webinar – Planning for the New Tax Year: Challenges and Opportunities from the Labour Government’s Budget

5 February Register now

To contact the team, simply get in touch via the Ask Us Anything form below.

Day to day technical support

Inheritance tax and wealth transfer planning

Online technical portal

Trust analysis service

European portability review service

The latest regulatory and tax developments

Product structuring to address specific client needs

The information presented in this briefing does not constitute tax or legal advice and is based on our understanding of legislation and taxation as of January 2025. This item has been prepared for informational purposes only. Utmost group companies cannot be held responsible for any possible loss resulting from reliance on this information.

This briefing has been issued by Utmost Wealth Solutions. Utmost Wealth Solutions is a business name used by a number of Utmost companies:

Utmost International Isle of Man Limited (No. 024916C) is authorised and regulated by the Isle of Man Financial Services Authority. Its registered office is King Edward Bay House, King Edward Road, Onchan, Isle of Man, IM99 1NU, British Isles.

Utmost PanEurope dac (No. 311420) is regulated by the Central Bank of Ireland. Its registered office is Navan Business Park, Athlumney, Navan, Co. Meath, C15 CCW8, Ireland.

Utmost Worldwide Limited (No. 27151) is incorporated and regulated in Guernsey as a Licensed Insurer by the Guernsey Financial Services Commission under the Insurance Business (Bailiwick of Guernsey) Law, 2002 (as amended). Its registered office is Utmost House, Hirzel Street, St Peter Port, Guernsey, GY1 4PA, Channel Islands.

Lombard International Assurance S.A. is registered at 4, rue Lou Hemmer, L-1748 Luxembourg, Grand Duchy of Luxembourg, telephone +352 34 61 91-1. Lombard International Assurance is regulated by the Commissariat aux Assurances, the Luxembourg insurance regulator.

Where this material has been distributed by Utmost International Middle East Limited, it has been distributed to Market Counterparties on behalf of Utmost Worldwide Limited by Utmost International Middle East Limited. Utmost International Middle East Limited is a wholly owned subsidiary of Utmost Worldwide Limited and is incorporated in the Dubai International Financial Centre (DIFC) under number 3249, registered office address GD-PB-05-04-OF-04-0 (Old No. 6), Gate District Precinct Building 05, Dubai International Financial Centre, PO BOX 482062, Dubai, United Arab Emirates and is a company regulated by the Dubai Financial Services Authority (DFSA).

Further information about the Utmost International regulated entities can be found on our website at https://utmostinternational.com/regulatory-information/ .

© 2026 Utmost Group plc